THE SPORTS GAME

Happy Thursday War & Peaceniks. Who’s got game?

Just in time for March Madness, we’ve surveyed Americans to find out how much sports they watch on TV, which sports they watch, where they get their sports, how they feel about paying for sports programming, and whether or not all the ads in sports piss them off. [We designed this survey with PCH Insights, who conducted this survey in 1Q of 2024. Methodology is below. You can download the entire report here.]

As pervasive as sports feels in our culture – the recent Super Bowl generated the largest audience ever for a TV program – as the chart above shows, only about half of us actually watches sports regularly. The record-breaking Super Bowl audience may have had as much to do with Taylor Swift as the game itself.

Additionally, as major league sports move from free broadcast to paid streaming, Americans ambivalence about subscribing to watch sports may have a major effect on how many people continue to watch these sports. Sure, the NFL dominated the airwaves last year, but will the audiences remain so huge, all season long, when fans are forced to pay to watch each game?

The data from this survey points to a cohort of rabid sports viewers who are very willing and eager to pay. But it also seems to demonstrate that as fees are charged, the TV crowds may get much smaller.

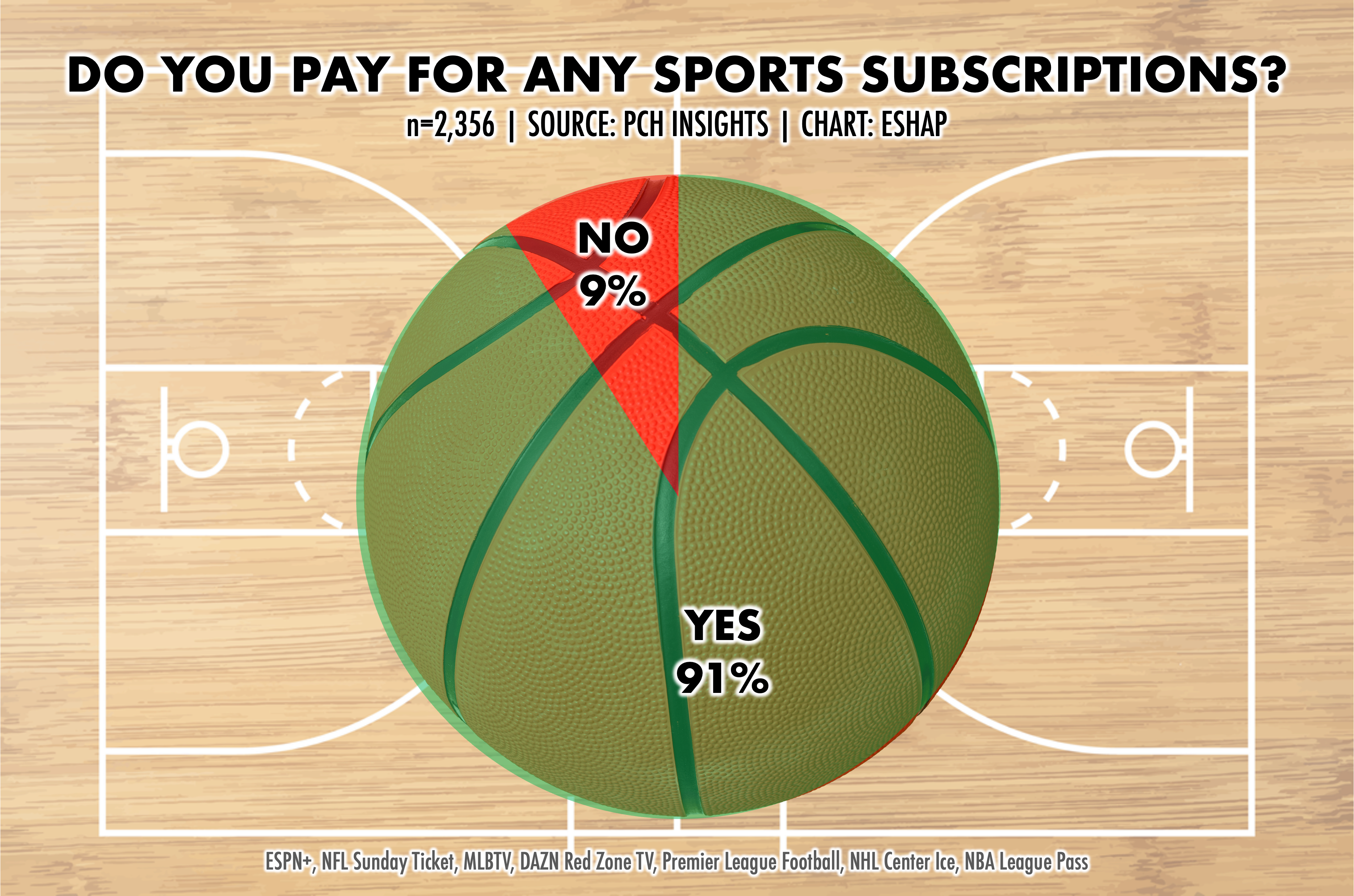

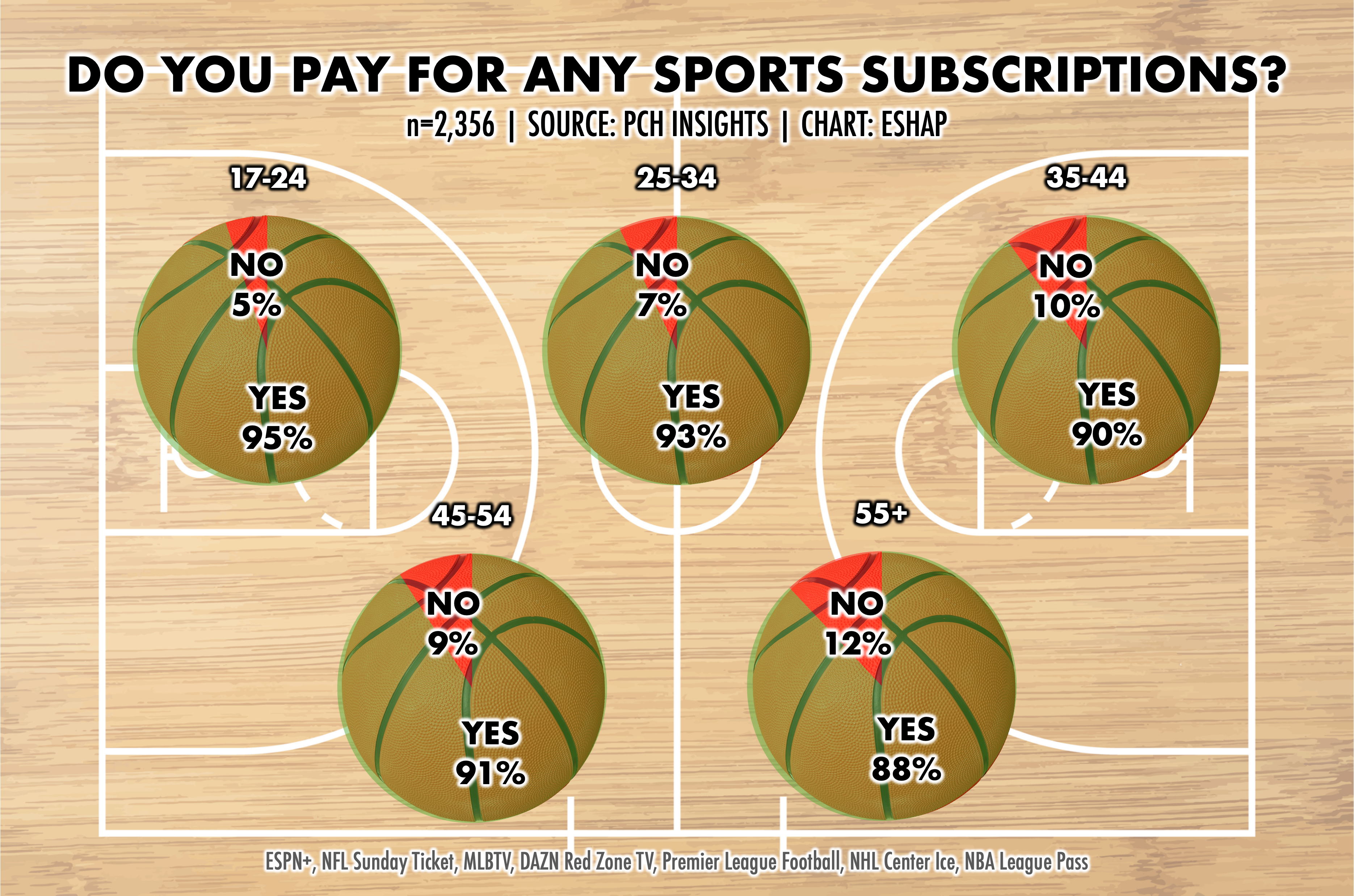

47% of Americans say they watch sports regularly. And a sizable percentage say they pay for a sports subscription of some kind.

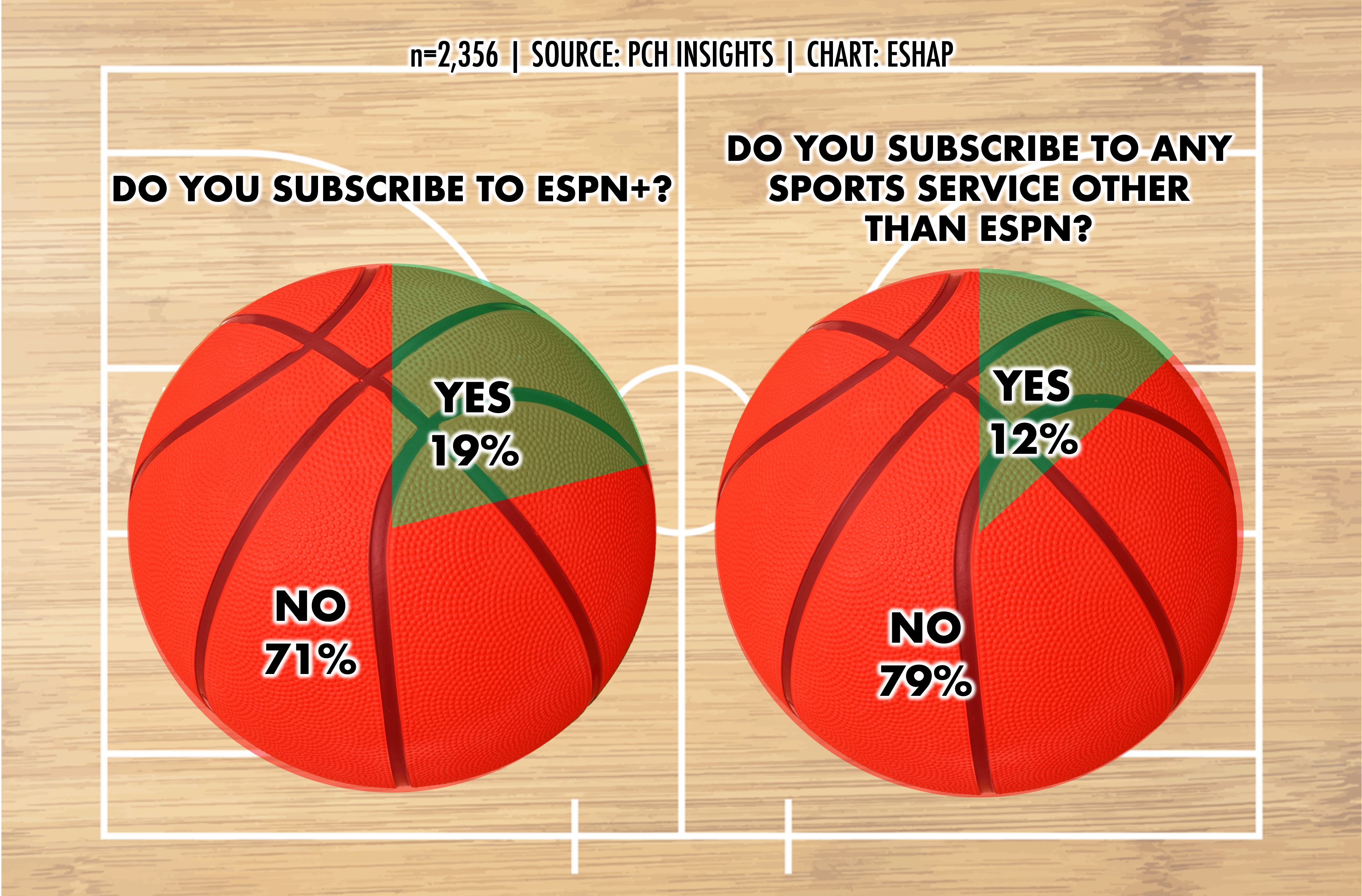

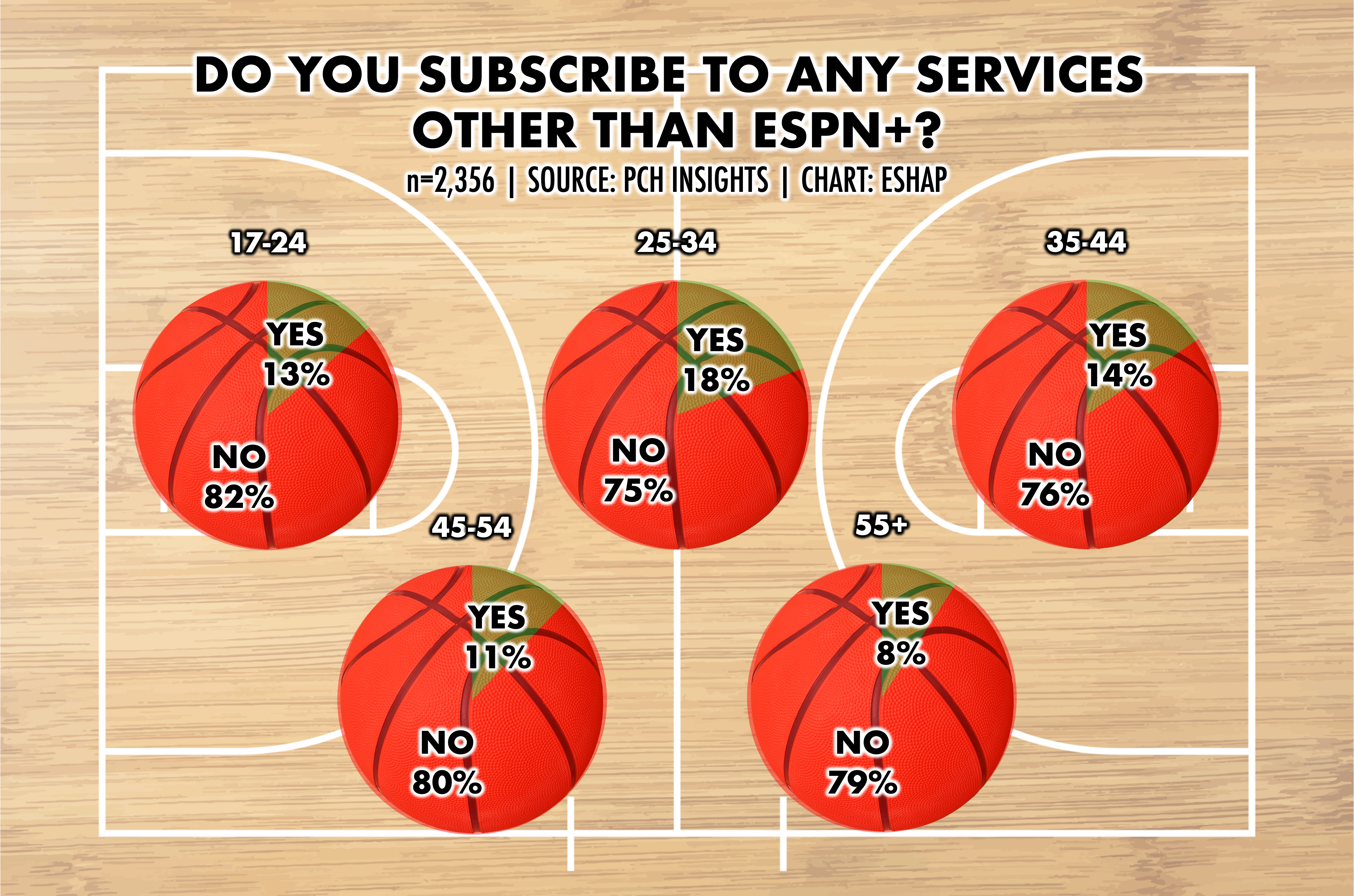

However, sports subscriptions are incredibly fragmented, with just 19% saying they pay for ESPN+, and 12% saying they subscribe to one or any of NFL Sunday Ticket, MLBTV, NHL Center Ice, NBA League Pass, Red Zone TV, DAZN, or Premier League Football.

As sports migrates from Broadcast to platforms like Amazon, DAZN, Apple, Netflix, and the soon to be launched combination platform from Disney, FOX, and WBD, this fragmentation will proliferate, as will the costs of paying to watch our favorite sports.

This begs the question: Will this create class system around major league sports, wherein only those who can afford to pay will be able to watch? Or, will out of home viewing become even more popular, with crowds at bars and other venues growing to emulate those at stadiums and arenas?

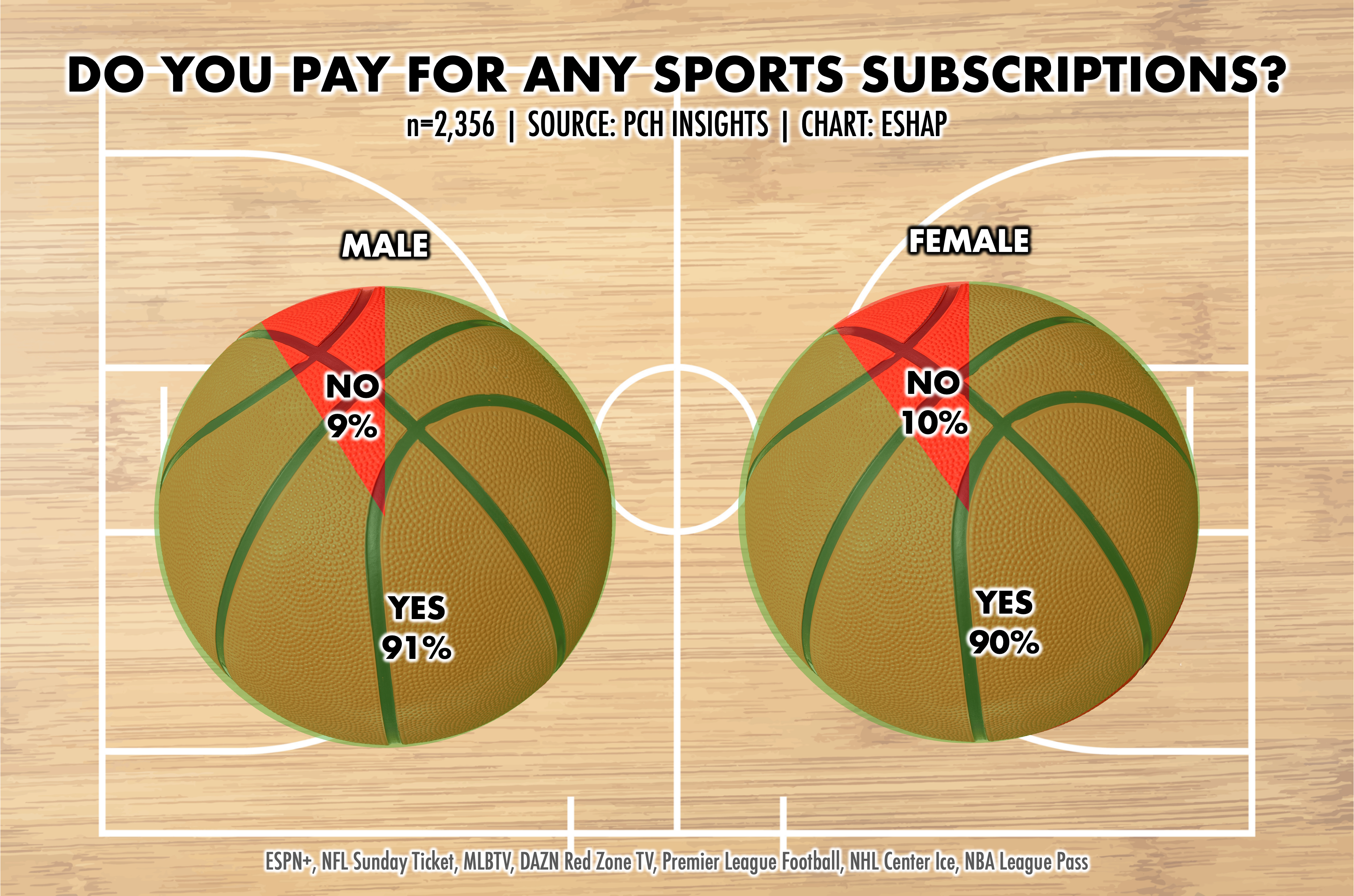

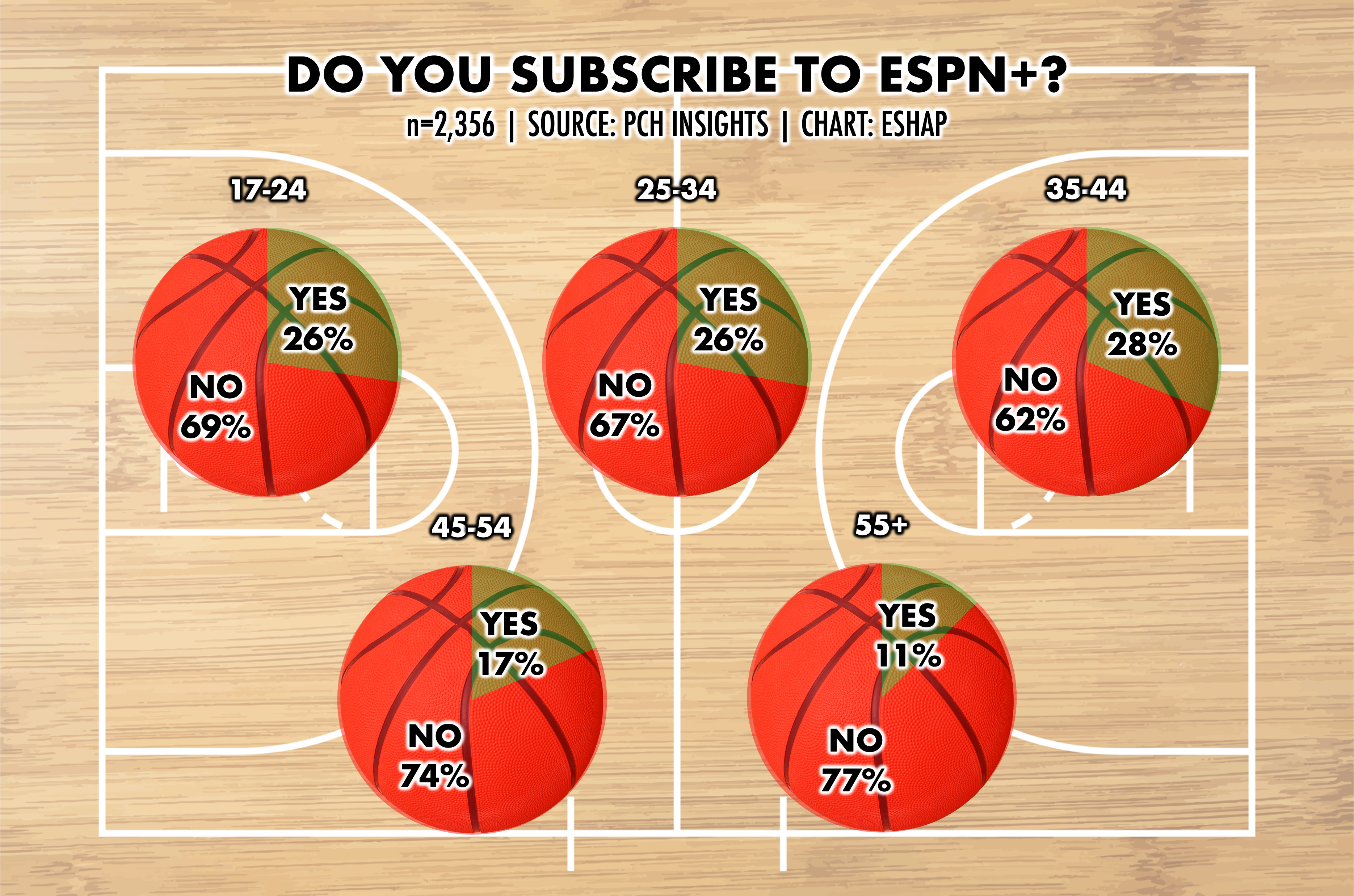

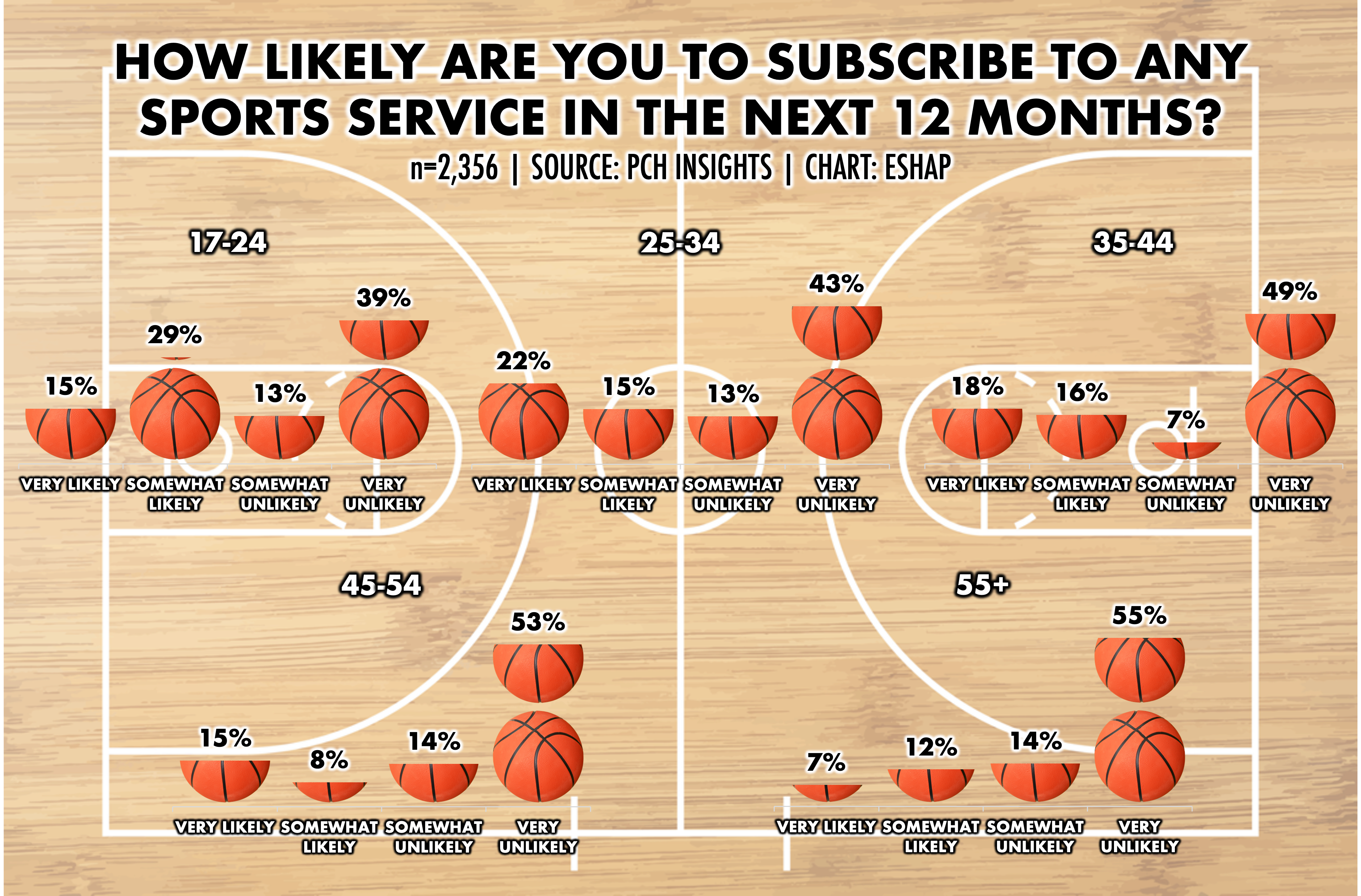

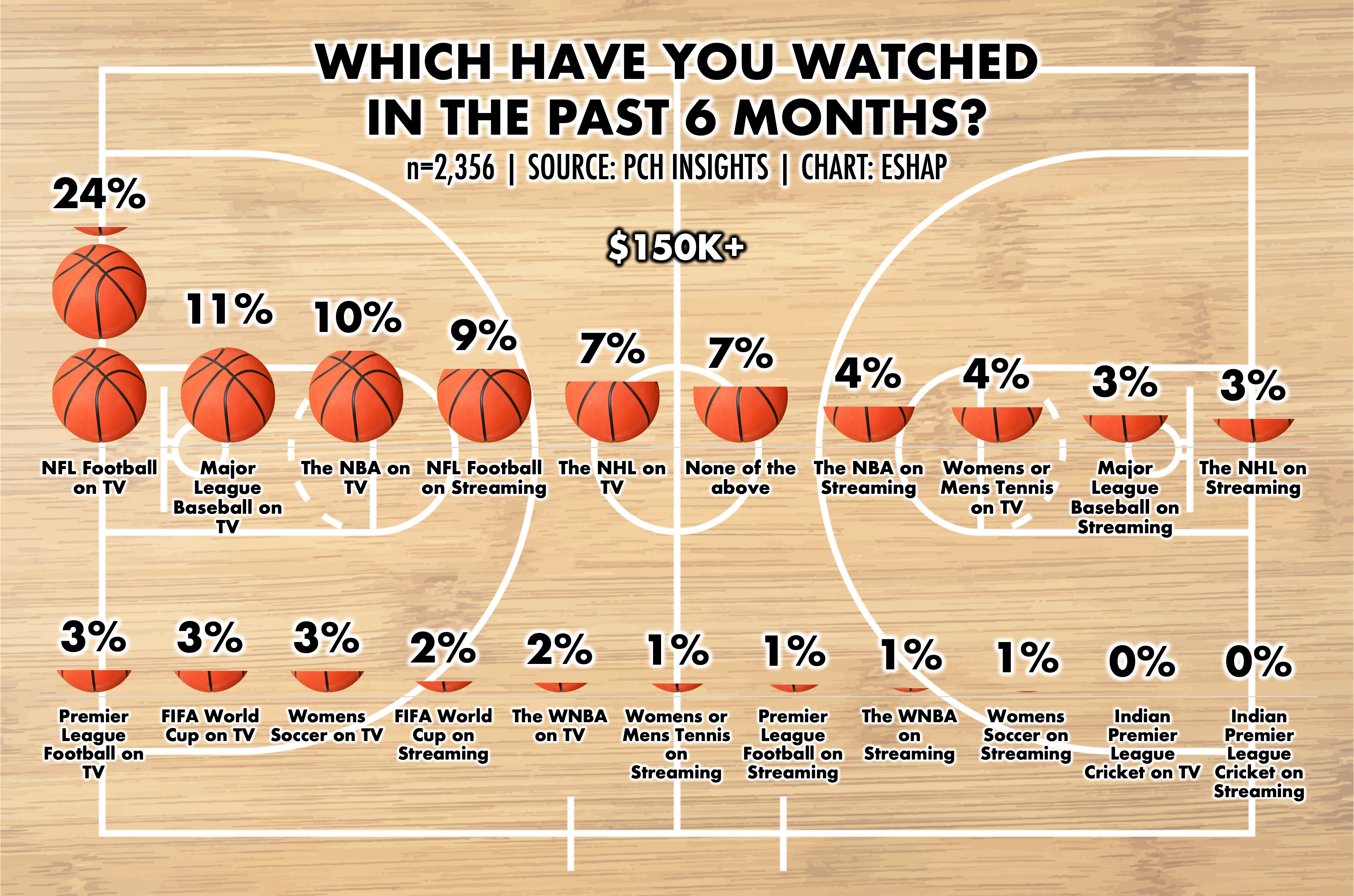

Younger consumers subscribe to sports (especially ESPN+) more than older audiences (reinforcing data that shows that younger consumers pay for more entertainment across the board than older). Higher income homes are much more likely to pay for sports (especially ESPN+) than homes with less income.

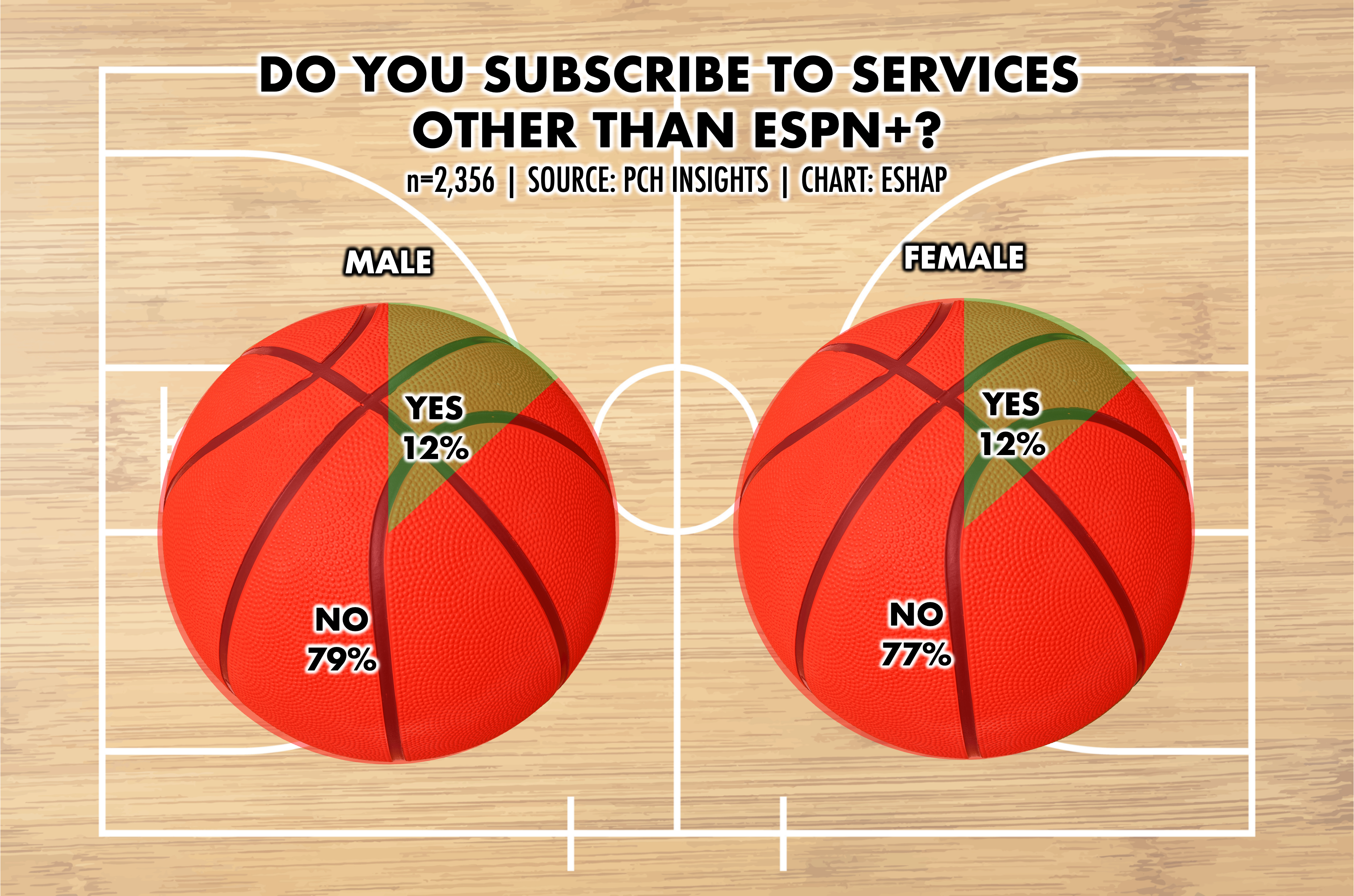

However, even in younger and higher income demos, no cohort pays for ESPN+ at a rate higher than 28%. This demonstrates substantial challenges for ESPN when/if they spin out from the cable bundle to a pure stand-alone streaming service.

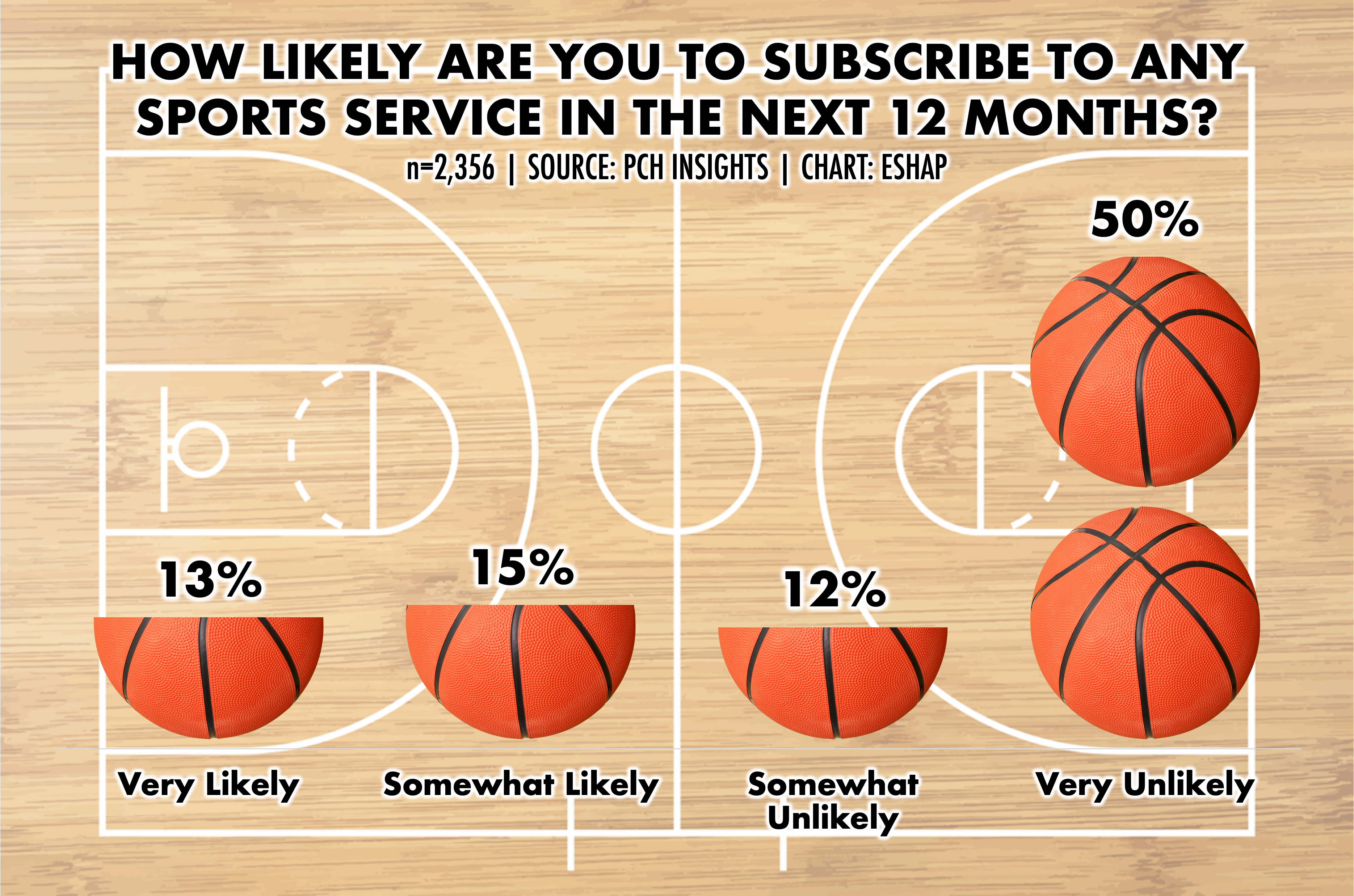

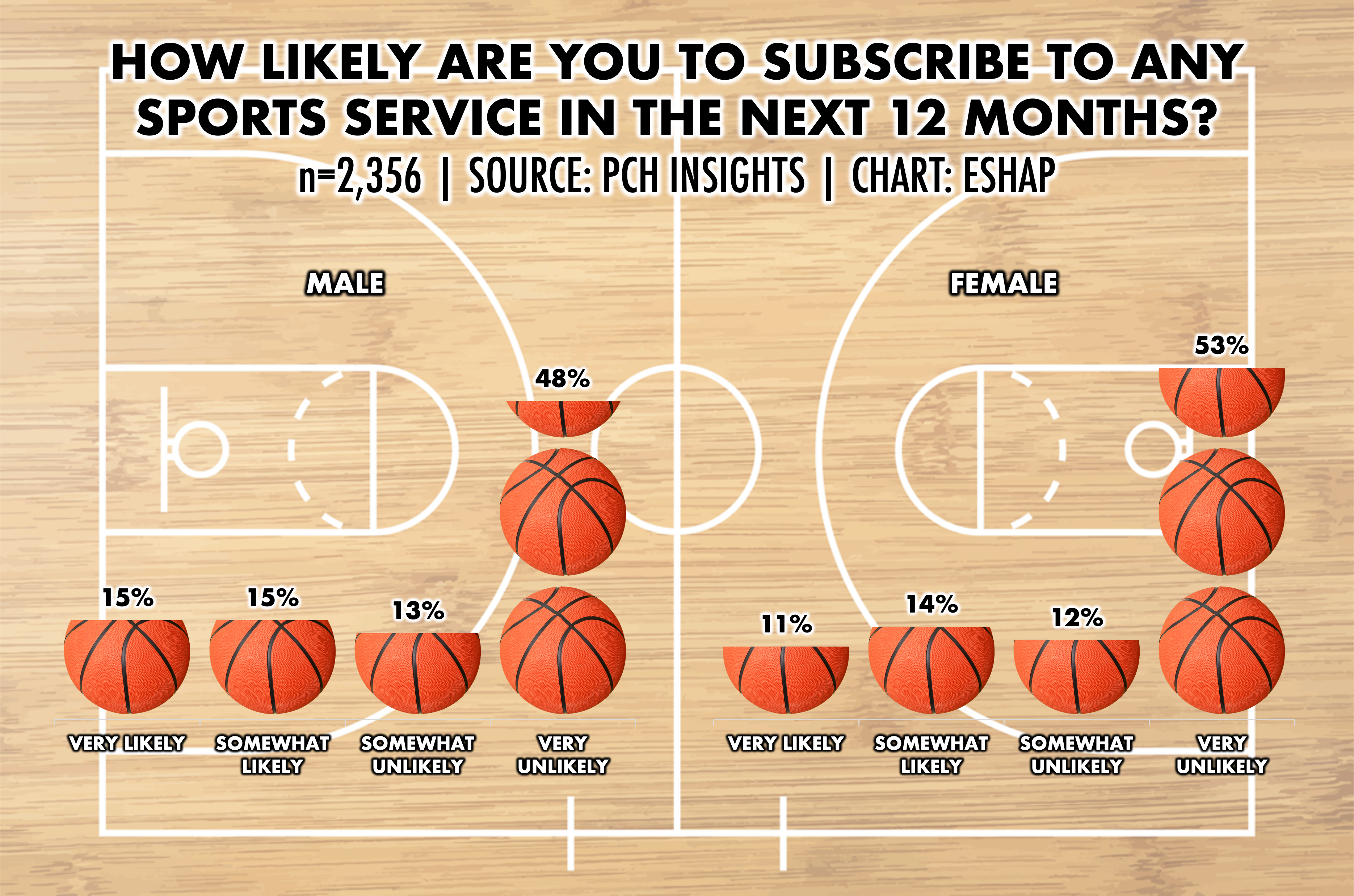

Most Americans are not likely to subscribe to a streaming sports service in the year ahead. While far more younger Americans are willing or likely to subscribe to sports services, consumers of all incomes say they are not in the market for new or additional streaming sports offerings.

This should be troubling for the new “Spulu” sports service from Disney, FOX, and WBD. Conversely, this could mean that American subscribers are getting used to the fact that their existing streaming services – Amazon, Apple, Netflix, and YouTube TV – are adding sports to their current offerings.

This seeming lack of appetite more paid sports services could mean that consumers are getting subscription and price fatigue – something with which all streaming platforms should be concerned.

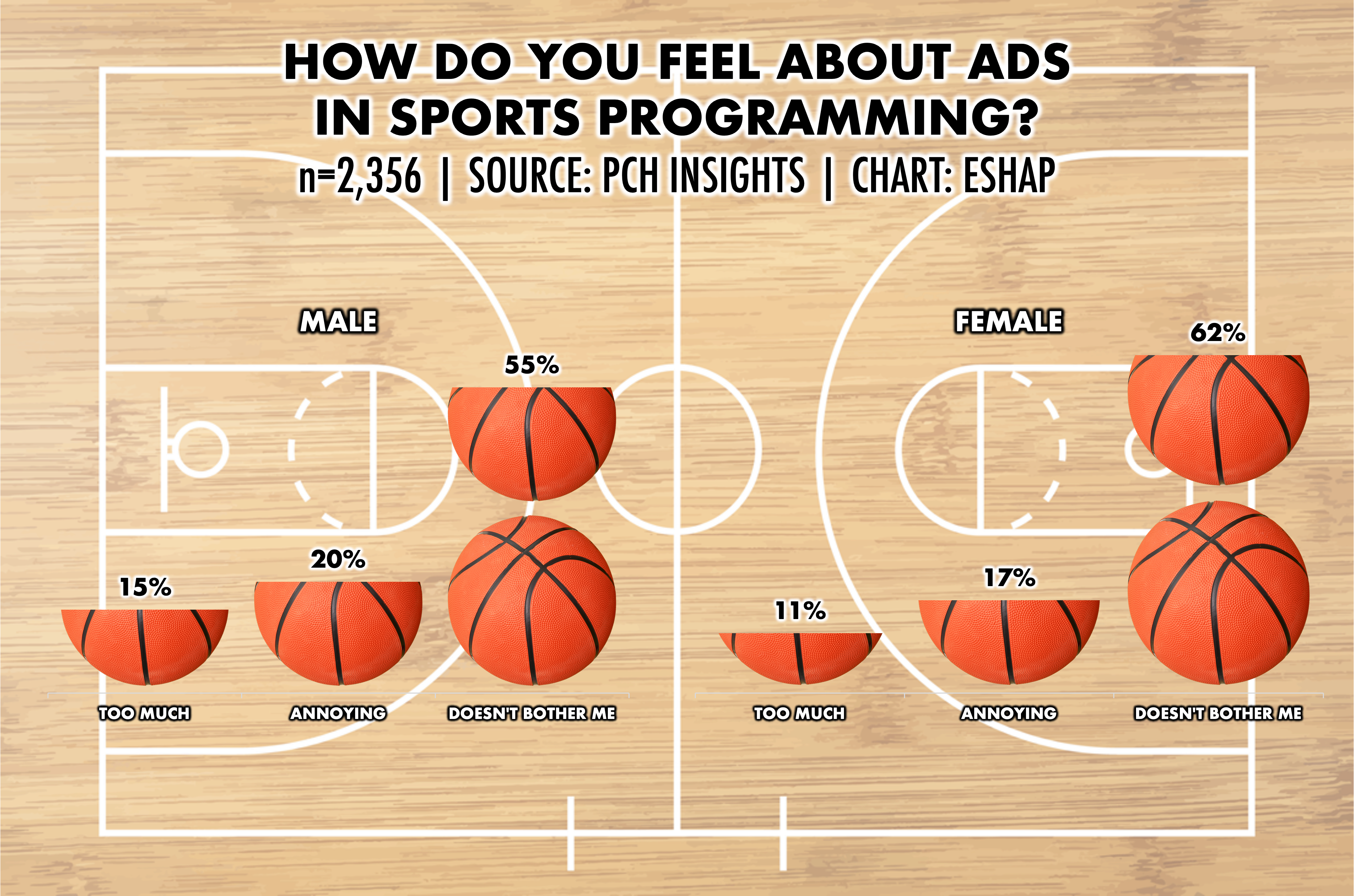

However, when it comes to the amount of advertising they see in their sports programming, audiences of all genders, ages, and incomes seem to be pretty satisfied.

Given that live sports is perhaps the best advertising environment on on streaming and television, this speaks well to the economic upside for platforms investing in sports programming and may offer them a viable way to maintain reasonable subscription prices, while still generating a return on those fees.

Interestingly, younger consumers, who are the most likely to be willing to pay for sports subscriptions, are also by far those least bothered by the intrusion of advertising in sports programming. This seems to demonstrate a savvy understanding of the economics of the entertainment they consume, due to living through the transformation of television in real time in their formative years.

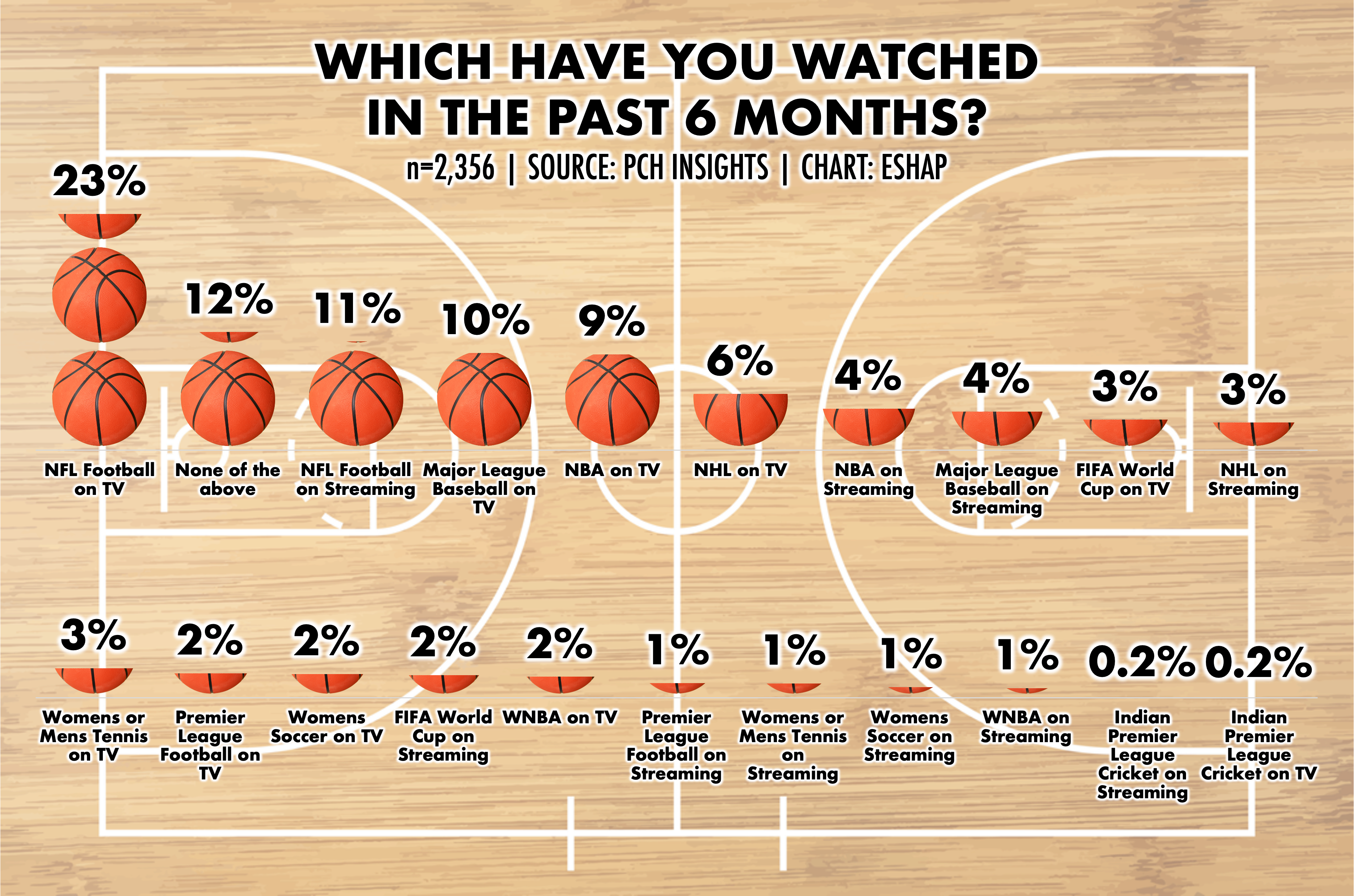

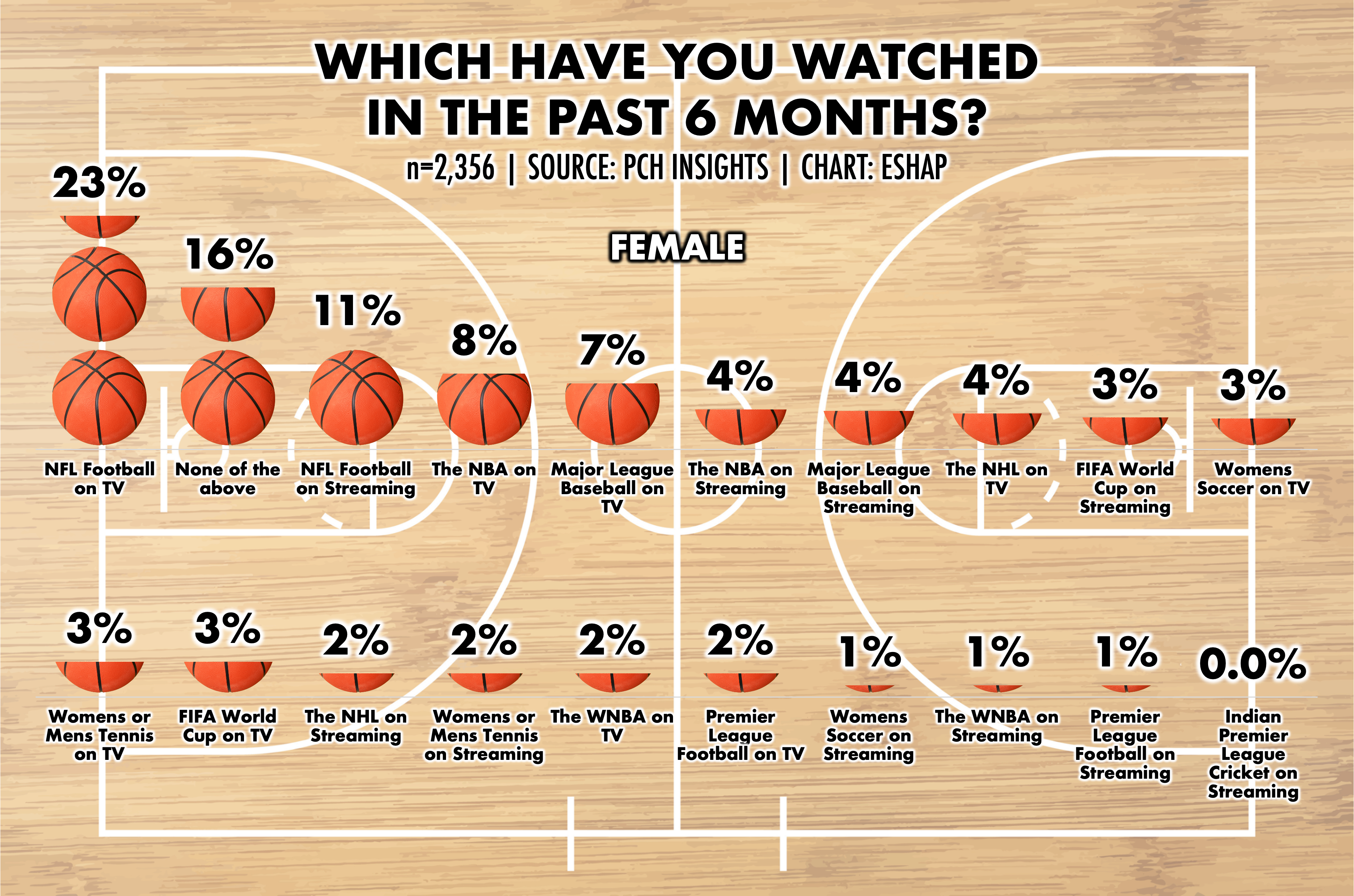

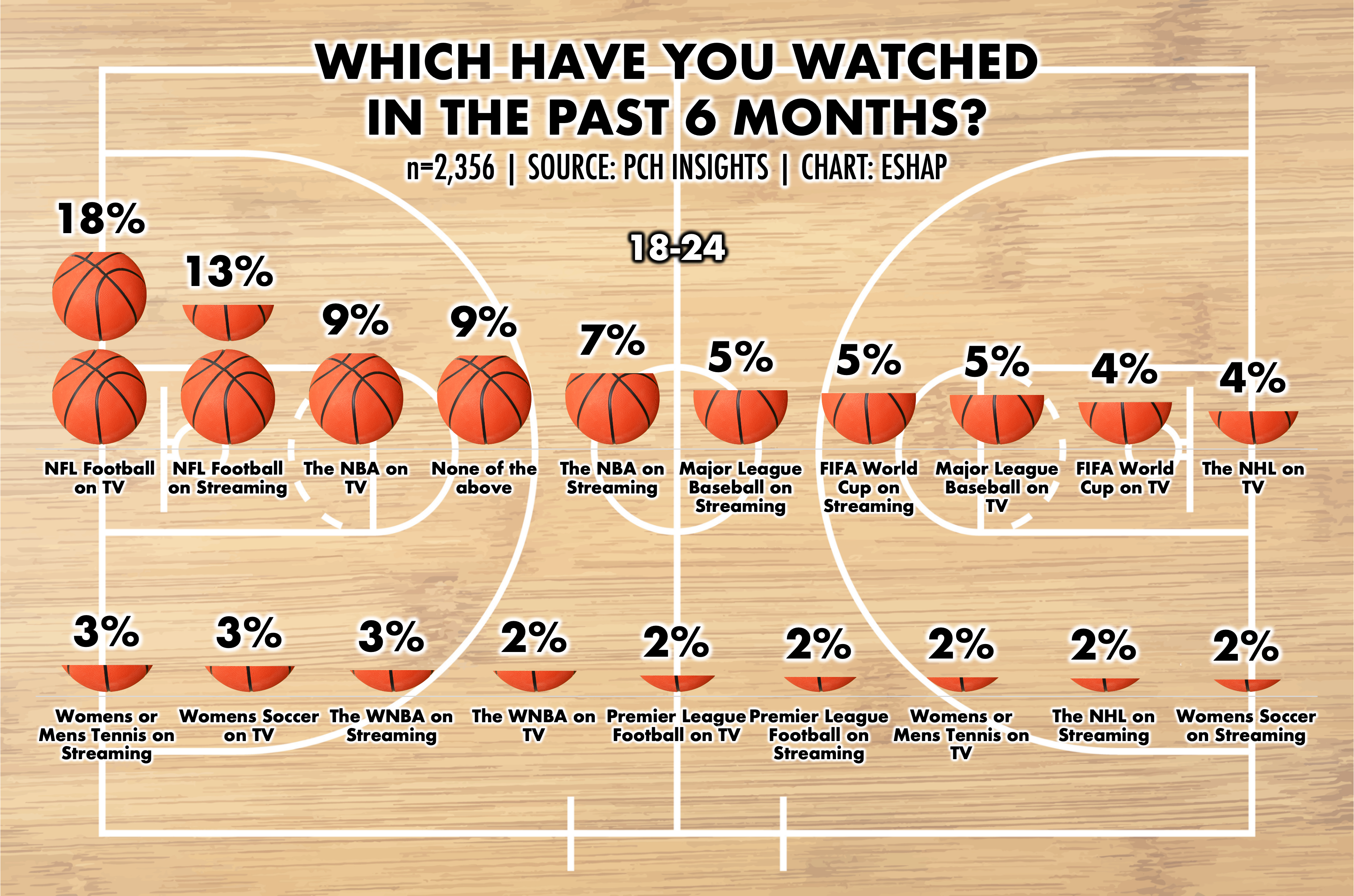

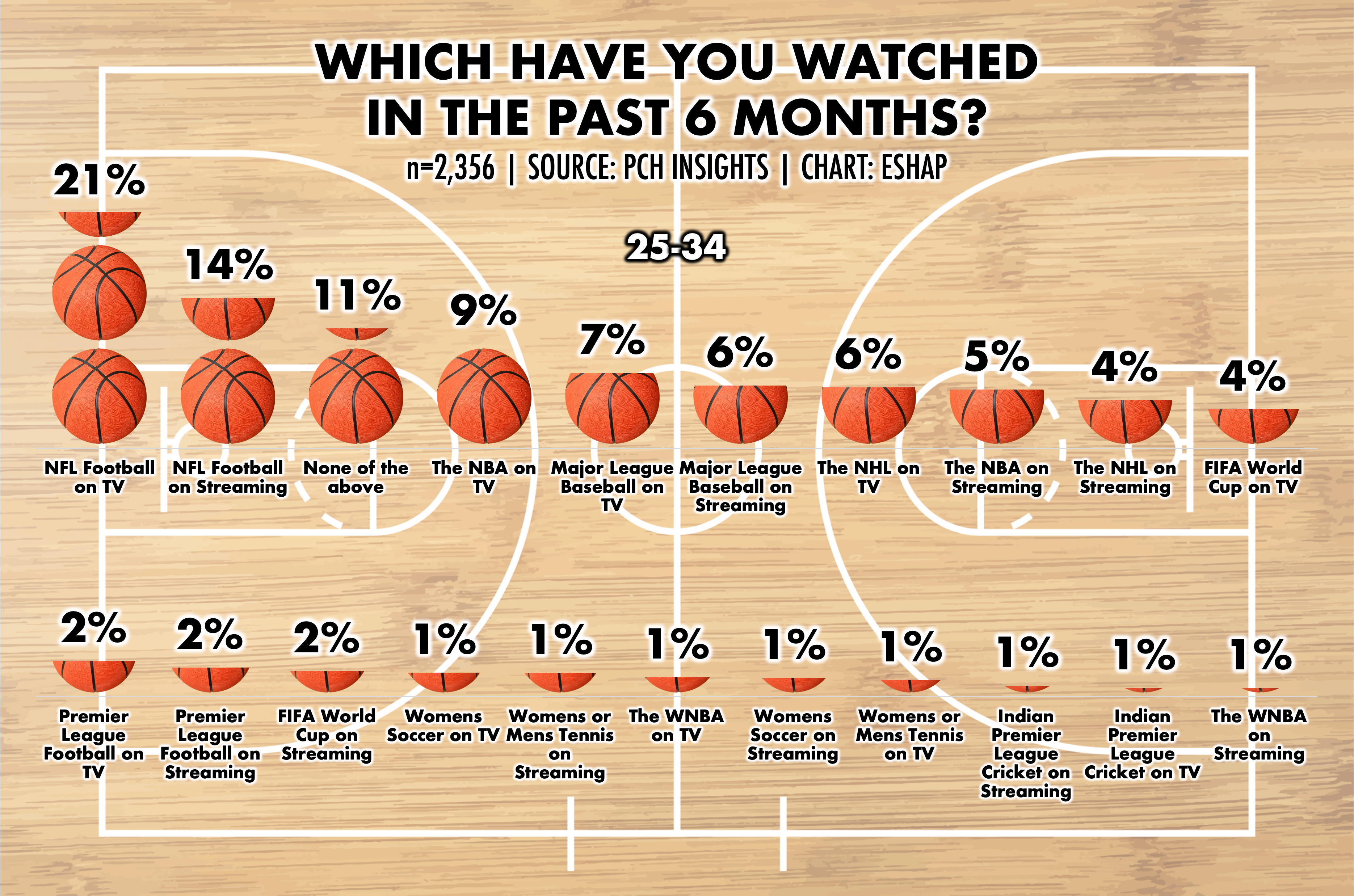

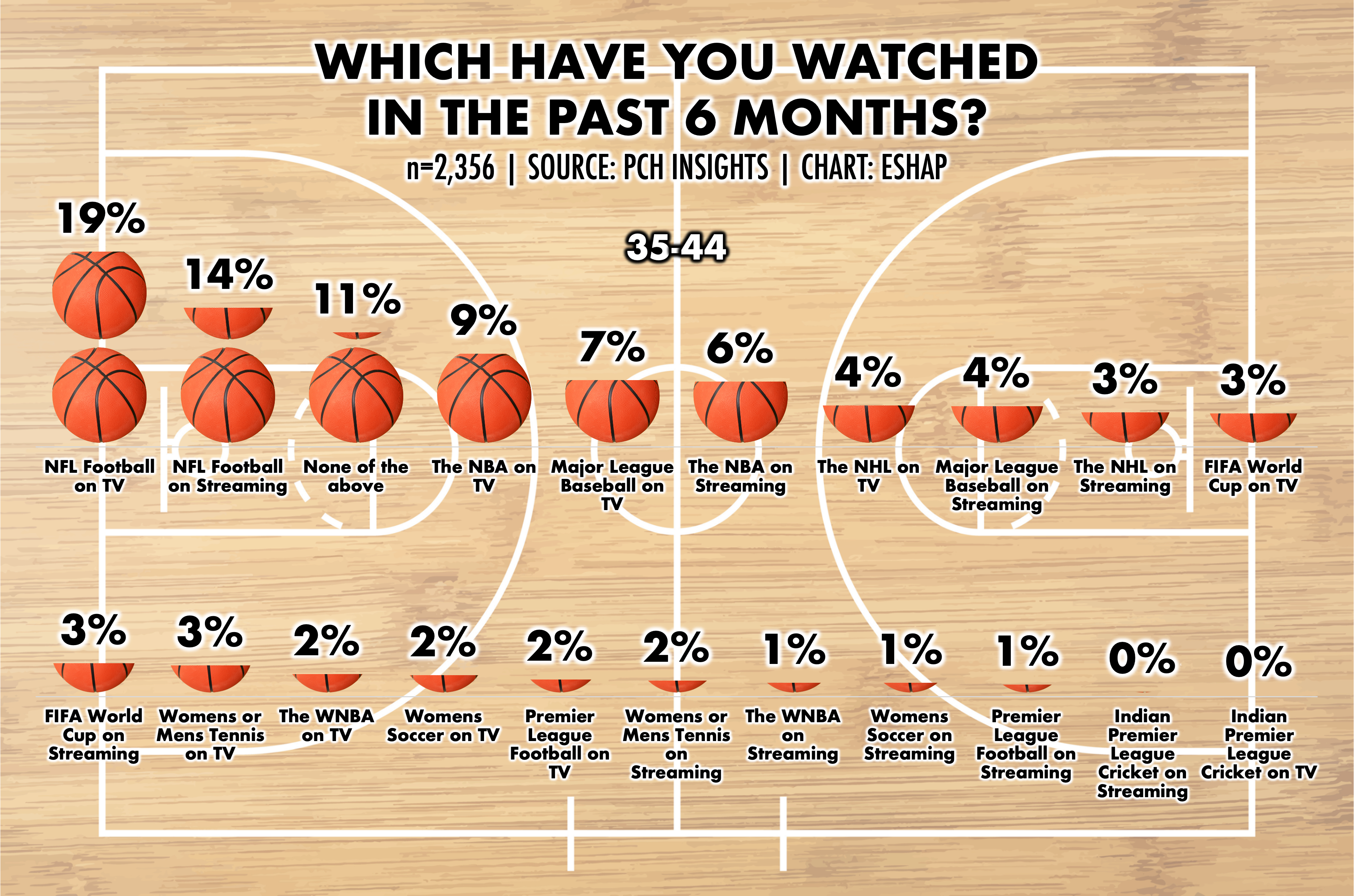

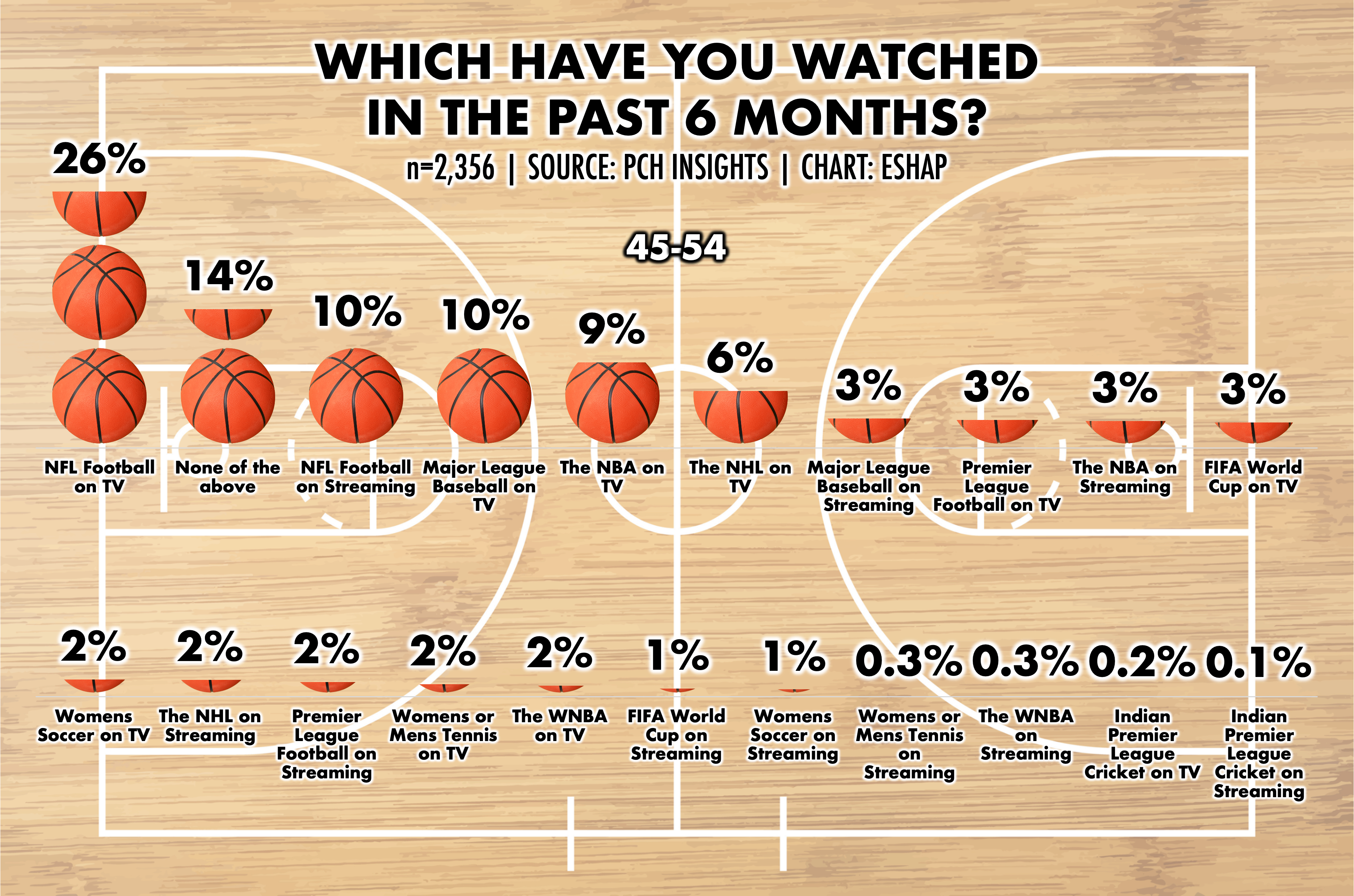

The NFL has the largest audience, across all demographics and incomes, in the US. NFL Streaming is now more popular than all other sports on TV. Yet, despite an audience that crosses all household incomes, the NFL’s core audience seems to be aging. While Taylor swift may have helped in that regard last season, this graying of the NFL fanbase is something to keep an eye on.

The fact that less than 10% of Americans watch the NBA on TV should be concerning for the league, given their upcoming television rights negotiations.

The number of viewers who say they’ve watched Major League Baseball on TV in the last six months may have more to do with the survey’s recency to the World Series than any growth in popularity.

Of particular note is the lack of television and streaming coverage of Women’s sports. Women’s sports makes up about 40% of all competitive organized sports, but makes up less than 5% of televised sports coverage. This is particularly notable, given this past Monday’s Elite Eight matchup between the Iowa Hawkeyes and LSU Tigers, which set a record for Women’s NCAA basketball, with an average of 12 million viewers for the entire game, and a peak of 16 million viewers. Which begs the question: If more Women’s sports were shown on TV and streaming, wouldn’t more people watch?

The big takeaway from all this data on TV sports however: As pervasive as sports feels in our culture, most sports are relatively local and niche.

The sports subscription game has obvious advantages for publishers, with built-in and highly engaged fan-bases, many of whom are willing to pay richly to access their favorite games and teams, and who return weekly and yearly for the sports content they love.

But sports rights are bigly expensive, and the fees are being bid up by streaming players with economic models very different from traditional media. As these fees get passed to consumers through higher subscription costs, price and subscription fatigue appears to be a growing factor in the lifetime value of those paying subs.

Despite pervasive sponsorships and ad breaks that elongate televised games, viewers seem to have a very high tolerance for ads in sports, giving the ad-supported model for televised sports room to grow.

The changing demographics of streaming audiences will have a major impact on the size of sports audiences and their willingness to pay for premium streaming services – with and without sports.

We designed this survey with PCH Insights, who conducted this survey in 1Q of 2024. Methodology is down below. You can download the entire report here.

Enjoy the Final Four and enjoy your weekend!

ESHAP

________________________________________________________________________

METHODOLOGY

This report represents an unbiased view of adults 17+ in the US from 2,356 weighted respondents. PCH holds a direct relationship with these respondents, who willingly engage in surveys as part of their strong engagement with the brand. PCH Consumer Insights recruited respondents from Publishers Clearing House's 15 million registered Audience Members, in 3Q 2023. The total responses were then weighted demographically to be in line and represent a US Census population.

When it comes to linear vs. streaming TV, sports viewing and advertising is likely to continue to hold on to old viewing and advertising modes. The natural breaks in play make advertising relatively tolerable, even as streaming subscribers feel a whole other level of frustration to breaks it in the middle of movies and tv programming.

I'm interested in what you think viewing will be like for the Paris Olympics — as opposed to the Beijing summer games in '22, the time difference is kinder to primetime viewing.

And as you noted, those "bigly" expensive sports rights are the wild card in how expensive watching our teams will become. Here's a breakdown I've been monitoring of where sports right are headed:

●MLB just renewed all of their broadcast deals in 2022 to expire in 2028

● NHL just renewed all of their deals through 2028

● The Premier League has a six-year deal with NBC that started in 2021 and runs until 2028.

● The NBA deal expires next year and potentially could line up here although the last deal was significantly longer in term.

● The UFC has a deal that runs from 2019 until 2024. The term of their new deal could potentially put them on the same timetable.

Hi Evan - great to see a piece focussed on sports.

What drives the drop-off between the first two charts? 91% pay for any sports subscriptions, but then only 19% and 12% respectively pay for the services listed.

Does the first chart capture cable subscriptions whereas the second only focuses on the streaming products mentioned? If so, can it be read that sports subs are still predominantly focussed in tradional distribution with slow streaming uptake? This would highlight the huge benefit the old school bundling model provided sports channels and subsequently the rights holders able to reap the rewards of large rights increases.