THE MAIN STREAM

Happy Friday War & Peaceniks! Ready for battle? Here’s your War Zone…

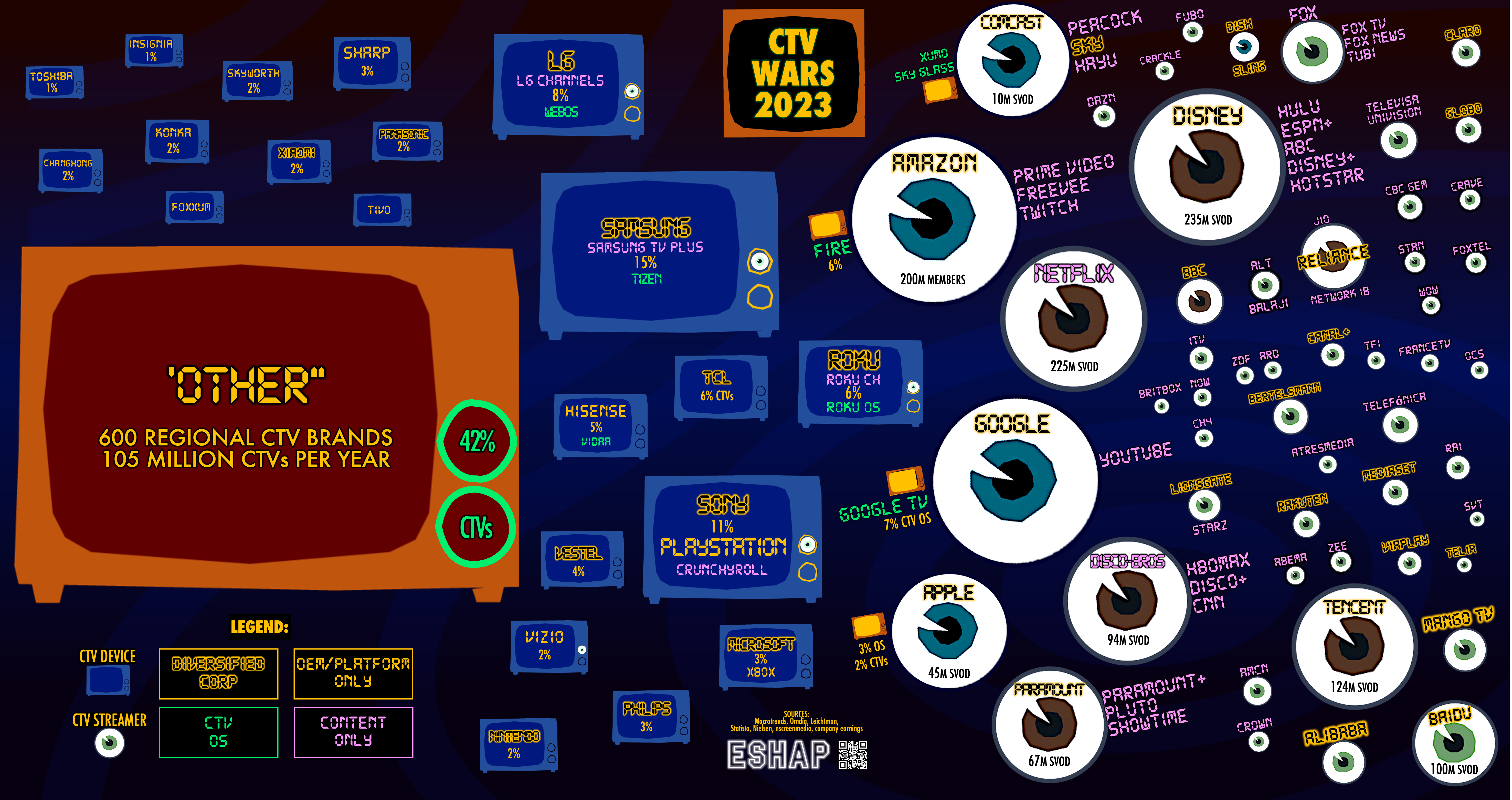

Above is my newly minted map of the CTV Wars. On the left are the makers and manufacturers of the world’s televisions. On the right are the publishers and platforms for our collected video content. Crashing headlong into each other in the middle are the folks who do a combo of both: from Samsung and their FAST platform Samsung TV Plus; to Google, whose Google TV is now the planet’s fastest growing CTV operating system (CTV OS) and whose YouTube just bought the rights to NFL Sunday Ticket.

As I said in this TVREV piece before CES, the most important topic in Media right now is the battle for control of your connected TV. The very next day, Roku announced they’re making their own TVs now.

This is a very interesting and perhaps fraught decision for Roku. On one hand, it seems like an unavoidable leap for the world’s biggest video streaming platform.

On the other, since nearly all of Roku’s streams come from just one market, North America, it’s a potentially dangerous move for a company that very much wants to install their CTV OS on CTVs made by other manufacturers like TCL and Sony, with whom Roku’s new TVs will now directly compete.

As the CTV Wars map demonstrates, 42% of the world’s CTVs (105 million units a year) are made by 600 smaller, regional “local heroes” who make and/or assemble CTVs in their territories but who shop constantly around for CTV OS partners to power the brains of those sets.

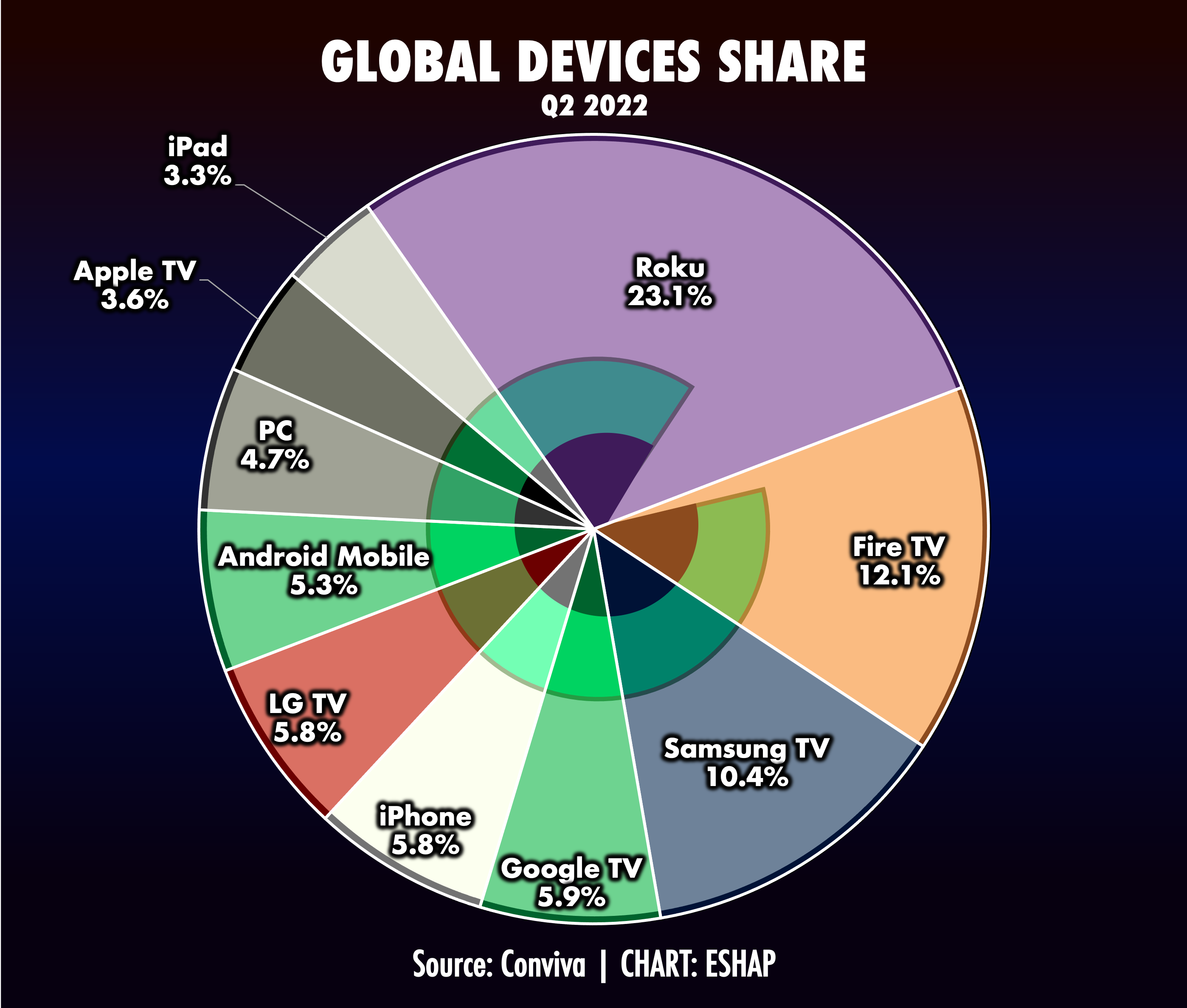

Regardless of what brand is on the outside of a CTV, whomever controls the CTV’s operating system inside also keeps the gate to monetization of the eyeballs that watch it. Samsung and LG, the world’s two biggest TV sellers, have their own CTV OS platforms. But despite that, combined, these two giants combine to sell just 23% of the world’s CTVs. Conversely, despite streaming 23% of the world’s video, Roku sells or powers just 6% of the world’s CTVs. That’s because, outside of the US, Roku has a very small footprint.

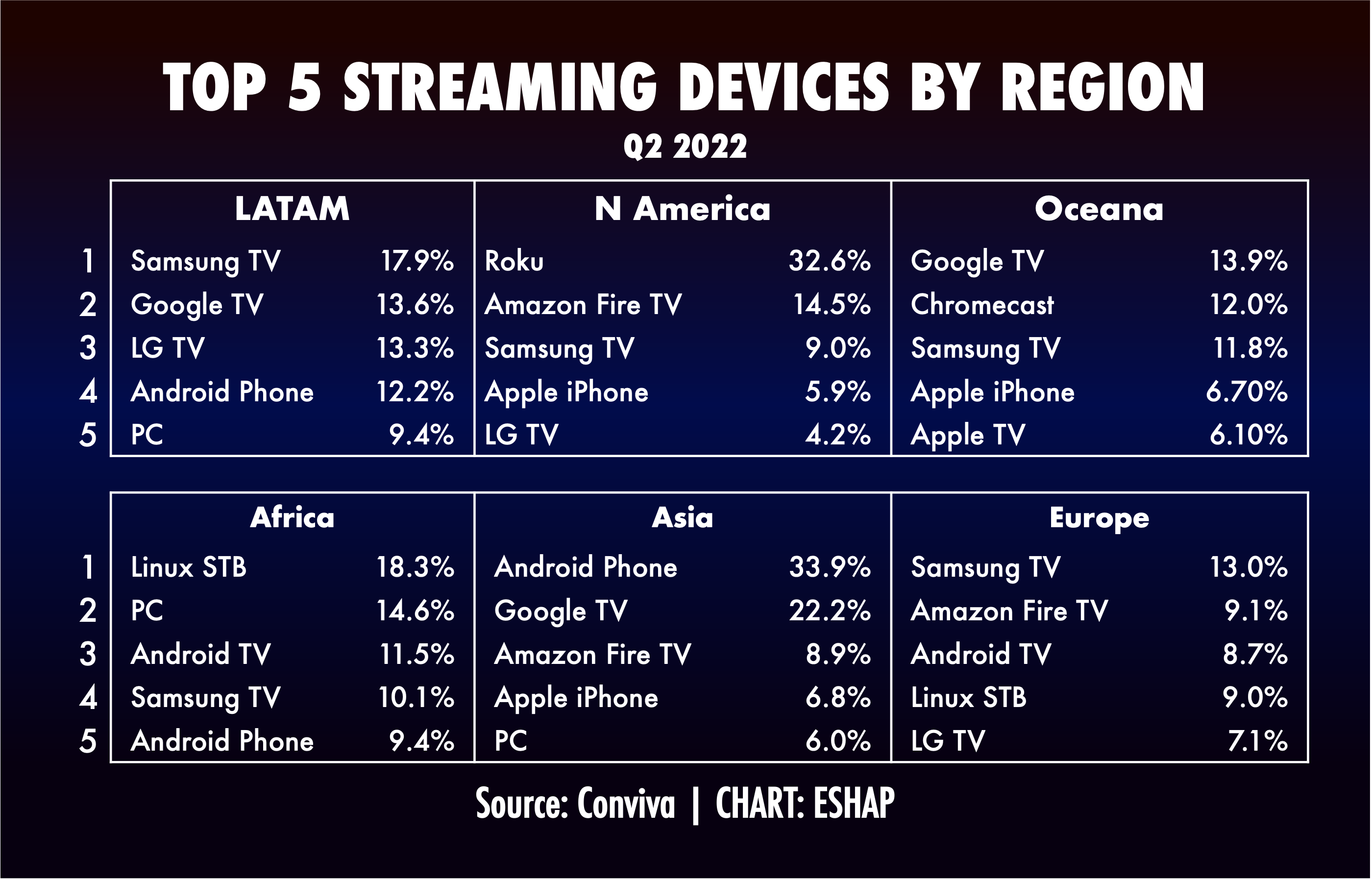

Meanwhile Google is picking up steam in regions around the world, controlling the top two platforms for streaming in Asia (the only region on earth where mobile video streaming has parity with CTV), and a top 5 platform in every region except North America, where their recent deal with TCL should put them in the top 5 by the end of 2025. Then there’s Amazon: Second in streaming in the U.S. and Europe, with their own Fire TVs coming in hot on the heels of their popular dongles.

Longterm incumbents LG and Samsung remain major players in every region, but there is a cap to the market share they can capture. Regional players are often protected by local tariffs and regulations, which often require that TV sets sold in-market must be made in-market. Thus these local heroes offer access to millions of homes to the likes of Google and their CTV OS, in exchange for fees from Alphabet for those eyeballs. And that’s why Roku’s decision to go into direct competition with regional players is so fascinatingly complicated.

On the topic of complicated relationships, on the platform/publisher side of the CTV Wars, players like Netflix, Disney, Disco Brothers, and Paramount must cross the CTV OS gauntlet to get their content, and their ads, to viewers. They do hold power in this battle (it’s nearly impossible to sell a CTV that does not have Netflix or Disney authenticated on its platform), but with increased competition, that power is likely fleeting. The map gets even more complex when you factor in Comcast’s new XUMO JV with Charter, and the unseen power of Walmart to make or break a CTV platform’s back.

On the other side of the pond, local platforms such as the BBC, ZDF, and TF1 should have enormous leverage with CTV players. While HBOMax, Netflix and Apple TV+ battle for subscribers month by month, regional broadcasters, with local content (and the local language), news and sports, are flat out irreplaceable must-carries. But only if they can truly cross the digital divide and take what is rightfully theirs. That’s why the BBC’s announcement that they will abandon broadcast and become a purely digital single-feed by 2030 should be a clarion wake-up call for all their peers.

The fight for control of CTVs is the seminal battle in Media for the next few years.

Connected TVs have become the home screens of our homes, gateways not just to video, but also much of our Gaming (Media’s largest market) which is migrating from consoles to the cloud; and ergo, direct to our big screens. This gives the CTV Wars added urgency and enormous stakes, with hundreds of billions in ads, subscriptions and commerce at stake.

On Tuesday January 17, at 1p PT/4p ET, I’ll be holding a webinar focusing on the CTV Wars. If you see the link and password below, thanks for being a premium reader! I hope you can join. If you don’t see the details, please consider taking advantage of the free trial, joining the webinar and then shutting me tf off.

In the meantime, enjoy the weekend!

ESHAP

Keep reading with a 7-day free trial

Subscribe to Media War & Peace to keep reading this post and get 7 days of free access to the full post archives.