The King Is Dead

Who Gives A Sh*t?

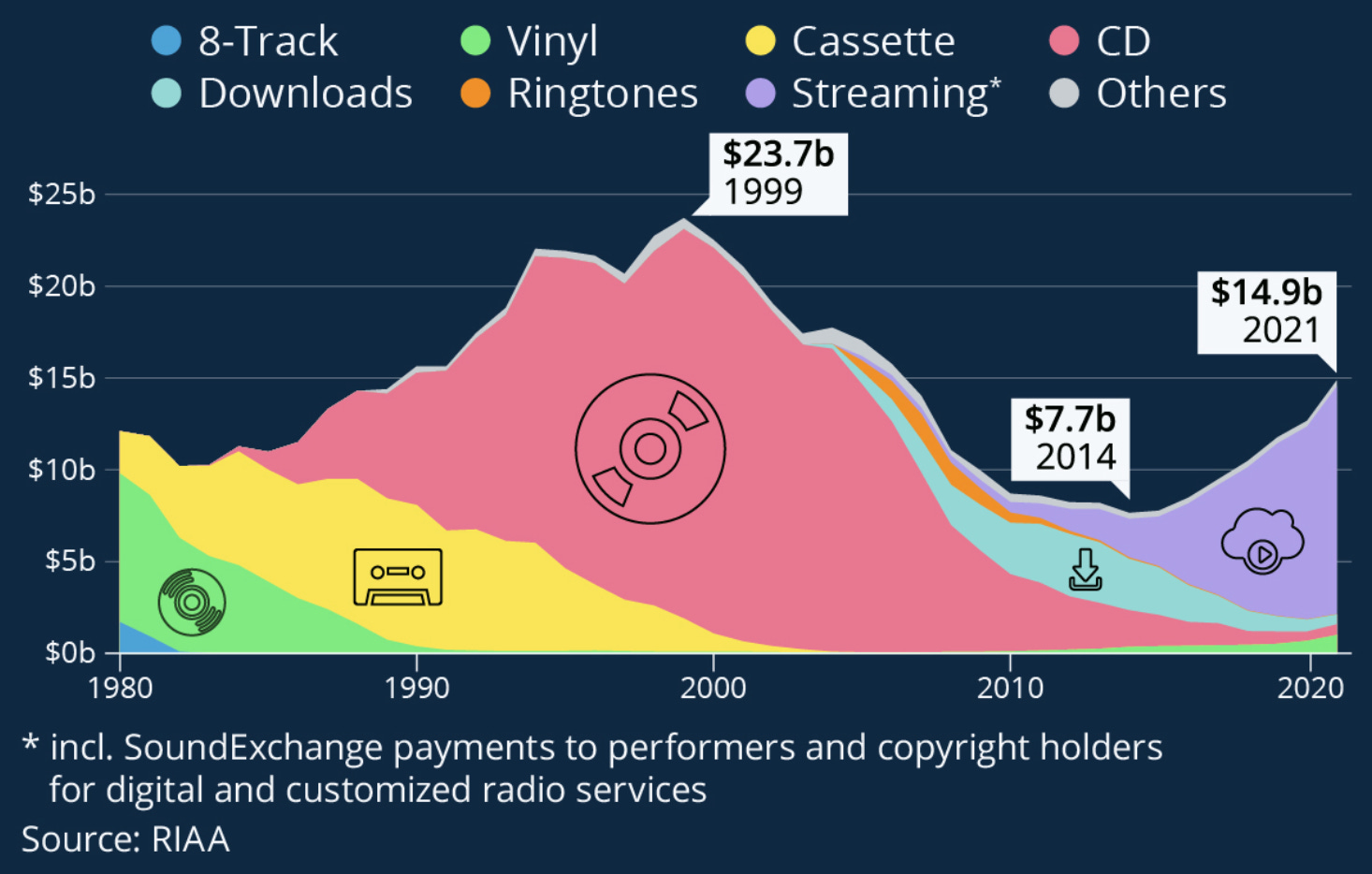

Happy Sunday War & Peaceniks. Let’s play Stream of Thrones!

Last week, I wrote that change has changed. Transformation is no longer a special event that we ramp up, plan for and announce! The rate of cultural and technological disruption (accelerated by the compression of time during our global lockdown) now requires constant, daily evolution. It forces us to wake up stupid every day, and learn new things as they happen, or face the risks of falling behind.

Embarrassingly, I personally fell victim to this on my last Media Universe Map! The new map I posted with that change piece last week included the incorrect number of subscribers for Disney Streaming. Beyond being inaccurate, I epically failed to properly memorialize a momentous moment in the Media Universe: in 2Q Disney surpassed Netflix as the King of all Streaming Subs.

Here is the corrected map:

Disney now has 221 million subs combined worldwide, to Netflix’s 220. And the lack of sustained fanfare around that moment is a perfect case study in how the rate of change in media has changed forever.

When Disney+ launched in 2019, the idea that they’d surpass Netflix in subs in just 30 months was unthinkable. Just a year ago, Disney claiming the Magic Kingdom in total streaming subs would have stopped our collective industry clock. This summer, when it actually happened, it barely registered as a blip on our radar. Why? By the time Disney caught Netflix, no one cared about the race anymore.

Lockdown sped the rate of subscription in 2020 and 2021 for every single service; as well as for free streaming TV. Then in 1Q 2022, as personified by Netflix, premium SVOD peaked. Immediately, the entire industry shifted its focus, ferociously.

Sure, Netflix relented on its ads allergy. More importantly though, that moment inspired the entire streaming ecosystem to veer away from sheer subscriber scale, and toward profits first.

Disney gave up streaming rights to Indian Premier League Cricket, while paying handsomely to retain the TV rights. Disney CEO Bob Chapek’s calculation is that streaming Cricket subs cannot generate enough revenue to cover the enormous jump in streaming rights. Or perhaps the $2.5 billion saved on Cricket streaming went to pay for huge jumps in fees for the NFL and F1. This may make sense, on paper, at the moment. However, we need to remember that Hotstar is 45 million of Mouse House’s 222 million subs (20%). It remains to be seen what will happen when (not if) Disney loses millions of devoted Cricket subs in India.

No one reacted to SVOD’s 1Q tipping point more violently than the Disco Bros. They are now infamously cutting everything to the bone in search of a white whale, aka $3 billion in savings mandated by John Malone in order to justify the massive merger. Unfortunately the cutting of overhead, head count and content has precipitated a 49% drop in market cap since the merger was finalized - a loss of $19 billion in shareholder value.

Elsewhere, despite a record breaking upfront, NBCU is cutting $1 billion from their budget, and floating the idea of eliminating their 10 o’clock programming.

Few have analyzed Netflix’s lack of foresight more harshly than me. And few have predicted a looming ad recession more loudly. BUT avoiding Netflix’s mistakes and storing budget nuts for a long cold winter are not longterm strategies. Focusing on profit margins, above all else, is a simple retread of the OG Media mindset that got them disrupted in the first place. It ignores the most important lessons about how our media has changed since Disney+ launched; and misses the message behind the media map.

Pay TV unwittingly colluded with its disruptors to destroy the Cable Bundle. Dissatisfied with only 40-50% profit margins, we sold our best stuff to Netflix, Hulu and Amazon, who offered cheaper platforms unchained from irrational pricing. Then publishers clawed back their programming to try and beat Netflix at their own game, without fully understanding the limitations of choice paralysis and subscriber fatigue.

Meanwhile, distracted by SVOD vs AVOD vs FAST, OG media lost track, as Apple and Amazon got busy building The Next Great Bundles: not TV bundles, but bundles of lifestyle needs. These companies are investing heavily - into recessionary headwinds, at a loss - to win and keep consumers inside their lifestyle bundles. The best example is Amazon’s simultaneous launch of Thursday Night Football and Lord Of The Rings as a massive branded content campaign for their new Fire TV/Alexa Speaker combo, and a magnet for a monster ad platform that by itself out-earns all of Netflix… powered by an unbreakable Prime Membership bundle.

Paramount gets it. Thus their bundle with Walmart+. Microsoft gets it. Thus their their coziness with Netflix.

Yet, many in media are reacting to Netflix’s slip-ups the way The Media tends to react to any new piece of information - with collective, overwhelming knee jerks. They are reacting to recessionary warning signs the same way. This explains why Disney’s Sub Crown got more of a shrug than a coronation. Unfortunately, it also demonstrates that most of the industry have not learned from the last 36 months, or their own history.

Yes, scale for scale’s sake IS a fool’s folly. BUT profit margin at the expense of investment, is NO MORE of a strategy than buying scale. Cutting deeply and indiscriminately into a recession, is a proven way to ensure your company will leave the recession weaker than when it started.

Blind faith in maximizing profits is what destroyed the music business at the start of this century. That addiction to profits above all else, combined with a lack of investment in new platforms, is precisely how TV disrupted itself and its business model.

When you take time to learn more about the next generation of customers every day, rather than focusing solely on how to profit most from each of them, it’s easier to invest in things that will make them more loyal and, yes, more profitable - longterm.

The Next Generation of consumers isn’t coming. They’re here. New models of serving them well can’t wait. There’s never been more data available to understand what they want. Netflix had clarifying data, a year before their really bad 1Q. They ignored it.

Media’s 2Q earnings were enormously informative about where the media is headed. Companies that diversify their revenue sources were able to offset segment downturns, WHILE investing in the future of their platforms. Companies chasing the market are hitting ceilings and running into walls. By over-correcting to not be Netflix and cutting their way to rosier margins, many are following the Netflix example and repeating OG media’s biggest mistakes.

Wednesday 9/14, I’ll being doing a webinar about how change has changed; why it matters; and what that means for media. Info is below. If you see it, thanks for being a Premium Sub! If you don’t, please consider taking the FREE TRIAL and joining us already!

Enjoy The Week.