THE HIDES OF MARCH

THE HIDES OF MARCH

How To Make Cuts WHILE Growing Revenues Without Winning Friends Or Influencing People

Happy Friday War & Peaceniks! Welcome to March Mapness (with a newly redrawn Media Universe Map for March 2023).

In the Media Universe, 1Q 2023 has had more ups and downs than a roller coaster in The Wizarding World of Harry Potter™. Since January 1, Apple and Microsoft alone have gained and lost $600 Billion in valuation.

However, today’s focus is on the Streamers: specifically the four biggest pure-play-stand-alone content publisher-platforms, Disney, Warner Bros Discovery, and Paramount. How these four players handle 2023 will likely dictate the long-term futures of all four, and possibly the future of all pure-play-stand-alone content publisher-platforms.

(Note: Comcast is not included, as they are not a pure-play-stand-alone content publisher-platform, and have a far different hand to play. More on that here.)

A current view of these four companies, from 30,000 feet:

I encourage you to click and expand. It’s a box score for 2022, and, if you want to discuss these four companies, you should dig into these specific KPIs. Yes, there are other data to consider when measuring their health - subscribers, LTV, and ARPU. But, at this point next year, these businesses and their CEOs will be judged on these metrics.

Not because I say, but because they’ve said so.

DISNEY

“Shares climbed after Chief Executive Officer Bob Iger announced plans for a dramatic restructuring of the world’s largest entertainment company, including 7,000 job cuts and $5.5 billion in cost savings.” - BLOOMBERG

Disney just launched their ad tier on Disney+. Meanwhile, they are still oddly noodling the future of Hulu, which has the highest average revenue per user of all streaming media, because it is also the best example of premium SVOD with ads.

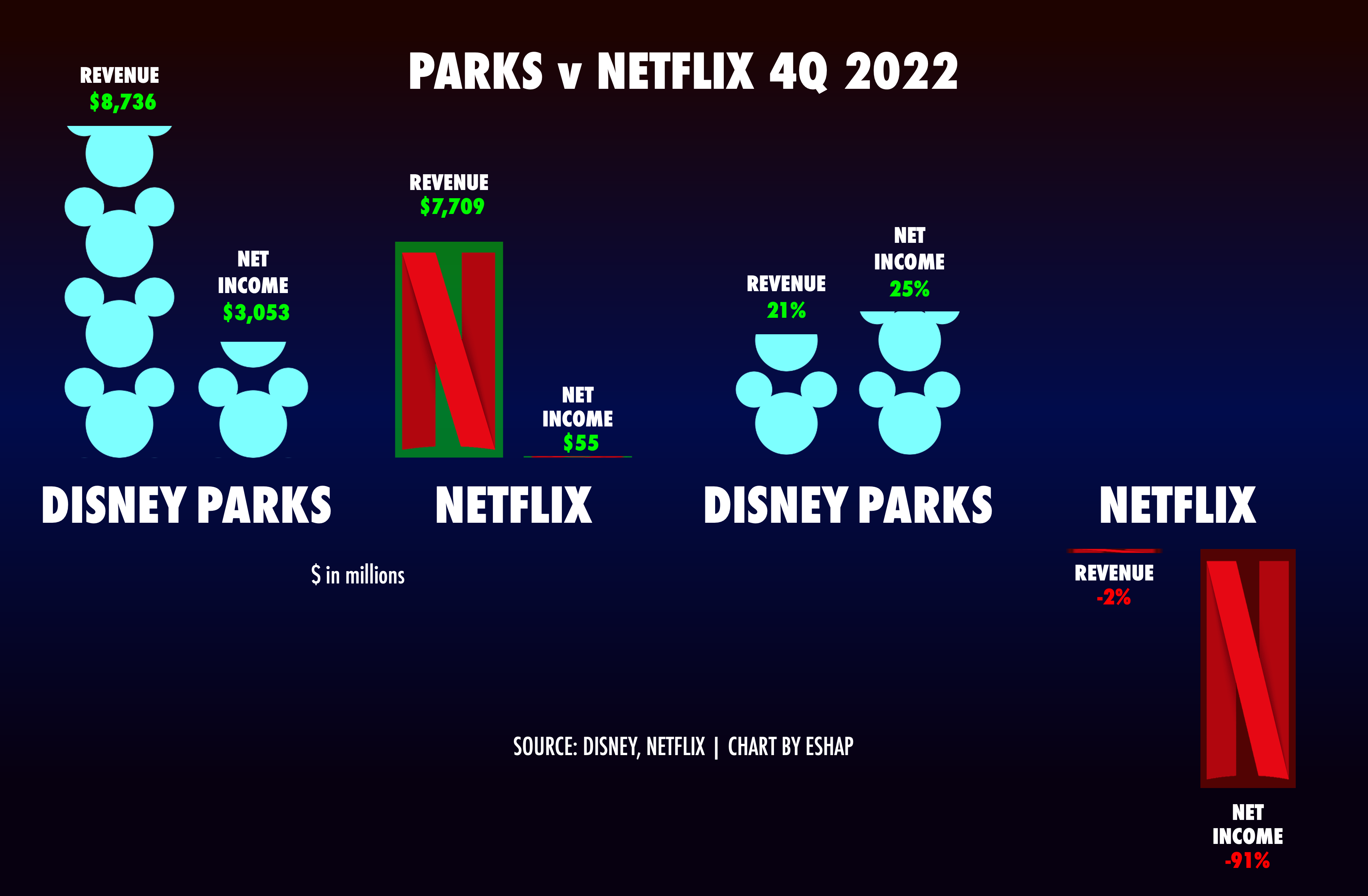

Meanwhile, Disney (alone in this cohort foursome) personifies the advantage of a diversified portfolio. Their Parks division was the driving force of their revenue and operating income growth in 2022, and will likely be so again in 2023. While the Mouse House lost the most in DTC of these four case studies, Disney also had by far the biggest total revenue growth - the only one of the four to grow operating income.

Disney does seem the best-situated to make the drastic expense cuts their CEO promised investors AND deliver revenue and profit growth, yet…

Hulu’s stickiness and ARPU are vital to Disney’s longterm DTC success, but it will cost them to acquire the rest from Comcast and to fully integrate the enterprise into the rest of their business. They have yet to fully invest in FAST, but they need to. Keeping/growing ESPN’s sports advantage will be uber pricey. Meanwhile, as their Parks prove, Disney would do well to look for more ways to diversify their enterprise around the lifestyles of their loyal consumers. Iger is considered a business genius for how he grew Disney during his first run as CEO. But remember: Old Bob did that by buying stuff.

NETFLIX

“2022 was a tough year, with a bumpy start but a brighter finish. We believe we have a clear path to reaccelerate revenue growth: continuing to improve all aspects of Netflix, launching paid sharing and building our advertising offering. As always, our north stars remain pleasing our members and building even greater profitability over time.”

Netflix started the premium streaming apocalypse a year ago, sending panic through the c-suites of Hollywood, and shoving all SVOD into a year of hand-wringing and head-scratching.

They spent the year scrambling to reinvent themselves into an ad business that doesn’t just care about scaling subs, and reimagining their massive content spend for this new destiny. Yet their ad tier is not ready for prime time (turning back ad dollars, signing up very few users), and it will require and enormous investment to get right. They still need to secure rights to insert ads into much of their most-watched content. This will cost billions. They still need to get the ad-product itself right. This will not be cheap. And, perhaps most importantly, they need to underwrite an entirely new slate of content initiatives - sports, news, live - to compete with the utility of other platforms going after the same exact ad dollars.

Netflix’s operating income fell 9% in 2022. But it plummeted 91% in 4Q, the same quarter they added ads. It will be at least another year (by their own admission) to see the full effect of advertising on their model. Meanwhile, they need to retool everything to compete on a global scale. This will make their cost-cutting/profit growth matrix that much harder to navigate.

DISCO BROS

“Is the Worst Really Over? Wall Street Hunts for Evidence of Turnaround Momentum in Warner Bros Discovery Q4 Results. With the restructuring and writedowns now largely complete, the company is now turning to execution, trying to right the ship in streaming in a push for profitability, while trying to keep its linear and theatrical businesses steady.” - The Hollywood Reporter

Disco Bros dance captain David Zaslav said “2022 was a year of restructuring, 2023 will be a year of building. And off we go!” He seems to be saying that “I’ve made all my cuts, now it’s time for profit growth!”

But WBD’s 2022 results are a petri dish for cutting expense drastically while trying to grow profit. They didn’t grow paying subscribers at all in 2022 and consequentially had the slowest DTC revenue growth of the four case study companies. Meanwhile revenue and income overall in every other segment fell, hard.

The Brothers Disco best epitomize challenge pure-play publisher/platforms face as they CUT EXPENSE while attempting to DRIVE REVENUE and PROFIT. Their ad business got hit harder than Disney and Paramount because they lack crucial, and expensive, programming elements.

Paramount and Disney have a TON of daily utility programming - sports and news - which offer them both enormous leverage in the ad market. Meanwhile, Zaslav is hinting at not renewing WBD’s biggest sports deal with the NBA; draconian cuts at CNN have decimated both morale and viewership, and their big pull-out from kids programming could be a major disadvantage over time.

Sure, they are (finally) getting into the FAST and AVOD business. Zas has said, “We can create a Tubi or Pluto without buying content from anybody, by just being able to put it out ourselves.” Neat! But there’s a dirty little secret about the FAST explosion that all players will discover(y) in 2023… To make FAST and AVOD truly work over time, and to compete in a hugely competitive ad environment, combatants will need to spend money on marketing, infrastructure, and (yes) programming.

Yes, WBD got out ahead of the austerity movement that everyone has jumped on since. But as 2022 proves, cutting is one thing, keeping those cuts in place WHILE ALSO growing revenues and profit is another.

PARAMOUNT

“Paramount CEO Bob Bakish vowed to return the company to earnings growth in 2024. ‘Our content and platform strategy is working and, with even more exceptional content coming this year, we expect to return the company to earnings growth in 2024.” - THE HOLLYWOOD REPORTER

Paramount had an amazing year in feature films, embodied by Maverick. They have PlutoTV, one of the strongest players in ad-supported streaming. They grew their paying DTC streaming subs by 10 million, and grew their total revenues 5% YoY.

And yet… Operating income was down 12% for the year. Theatrical will be a complicated business, with enormous risk (Maverick was an expensive investment that sat on a shelf for two years). PlutoTV is a big player in FAST, but it still requires both marketing and programming investments to convert today’s 78 million MAUs into regular viewers and reliable revenues (a challenge shared by all FAST and AVOD players, btw.) Crucially, they are clearly still figuring how to balance programming investments and belt tightening for their premium TV platform, as they manage the decline of their linear business.

This paradox is best embodied for the entire industry by Paramount rejecting offers of as much as $6 billion to buy Showtime on one hand, while slashing its budgets and mashing into clumsily-named subservience with “Paramount+ with Showtime.”

THE FOUR HORSEMEN

Each of these companies have promised loudly to BOTH dramatically cut expense AND grow revenue. That’s a near-impossible task under normal circumstances. But, after the SVOD Gold Rush of lockdown, these four horsemen find themselves on the front lines of a streaming apocalypse that will make the balance of austerity and aggressive growth a super hard needle to thread.

Every one of these four pure-play publisher/platforms is fighting with each other for the same exact slices of the Media pie: subs, viewers, and ad dollars. All four must also simultaneously compete for those same revenues with multi-faceted revenue machines like Comcast, and Big Tech Death Stars like Amazon, Alphabet and Apple - all of whom have alternative revenue levers to help balance streaming losses, and all of whom serve as gatekeepers our four horsemen case study companies need to fulfill their business models.

Which of these of these companies are best positioned right now to accomplish this herculean high-wire act of cutting to the bone while growing the body? Look at the numbers, from this height, and ask yourself: Which of these companies would you rather run right now?

Many people comment to me about how well WBD has managed their expense cuts, believing Zaslav’s spin about how well the merger (which has lost 50% of its value since merging) is working. Many folks believed Netflix’s spin about new subs and a new ad model, despite the fact that their year end performance was so bad that their CEO used it as his exit music.

Both Bobs, Iger and Chapek, faced some hard questions in their year-end earnings reports, but when you look at the box score, both Paramount and (especially) Disney seem far better positioned right now to cross the rubicon of 2023.

But, as 2023 is likely to prove, aggressively growing revenue while majorly cutting costs is even harder than it sounds. And for pure-play players, this balancing act is even harder. Each one of these case study companies must grow the newer parts of their businesses, as they manage the decline of linear. And, as few analysts or shareholders seem to notice, each of them should be looking for new business extensions to diversify their models and better compete with the massive players in the space.

WBD’s biggest hit of the year was actually game: Harry Potter Hogwarts Legacy. In just two weeks that one video game out-earned all three of the Fantastic Beast spin-off films.

In 2022, Disney’s Parks department saved their year, as it will likely do again in 2023.

So, as we end 1Q 2023, and take into account all the promises made during earnings calls by the CEOs of these four major Media players; the question really is not who can cut the furtherest while growing the most. The test for these players - and for pure-play content companies writ large - is how strategically these CEOs can cut, without cutting bone; and how well they each manage to continue to invest in future revenue generators, while improving their bottom lines.

Perhaps the sole question for all four (and streaming itself) is not how they do this, but if they can.

I’ll be speaking on all this and more at SXSW next week, and on a webinar for War & Peace paid subscribers on March 20. Info for the webinar is below. If you see it, thanks for being a paid sub! If not, consider the free trial so you can join in the fun.

I hope to see you in Austin or on Zoom!

Enjoy the weekend!

ESHAP

Keep reading with a 7-day free trial

Subscribe to Media War & Peace to keep reading this post and get 7 days of free access to the full post archives.