Must Have TV

Are Disney and Amazon becoming each other?

Happy Monday War & Peaceniks!

Jeff Bezos has done what no Bond Villain could: Captured 007. Last week, in one of the most anti-climactic endings in movie history, Amazon closed its deal for MGM, with not a peep out of the FTC, who had threatened an investigation of the deal that never materialized.

Assuming the fruition of this deal, I had moved the MGM icon into the Amazon orbit months ago. A week ago, I wrote that a challenge of this acquisition by Lina Kahn and the FTC would be bad for the FTC and for anti-trust regulation in general. Yet still, I found the quiet conclusion of this $8.5 Billion transaction for one of the world’s most storied film studios by one of the biggest conglomerates in human history somewhat surprising for its utter lack of fireworks.

In approving the deal, the EU’s antitrust commission declared that MGM’s content could not be considered “must have.” The slate includes two huge franchises: James Bond and Rocky. And yet, it’s hard to argue that buying one of the original big six Hollywood studios offers Amazon any significant advantage in the marketplace that it does not already have.

This was amplified this past week by a separate ruling about Amazon’s entertainment business from a major arbiter of media relevance, Troy Aikman. Aikman, one half of the longest standing play-calling duo in the NFL announced last week that he and Joe Buck would be leaving Fox Sports for Monday Night Football. Speculation had been that Aikman and Buck might be lured to Amazon’s Thursday Night Football when it goes exclusively to their platform this season. In turning down the box of smiles in favor of the Mouse House’s ESPN, Aikman said something that’s not oft heard: Amazon is just too small for him.

Part of Aikman’s decision to bring his talents to Monday Football on ESPN over Thursday Nights on Amazon is the desire to be a part of Football history: taking over arguably the most iconic franchise in TV sports. Also, Thursday night games do not get the same kind of quality matchups as Monday Nights, ergo cannot guarantee the same built-in audiences. But in Aikman’s comments we hear a desire for relevance. In his decision, we see Aikman has judged Monday Night Football “must have.”

For Amazon, both Troy Aikman (despite not landing him) and James Bond (now that they have him) represent significant strategies in building a “must-have” content portfolio modeled after the IP building master, Disney, giving their loss of Troy to ESPN an ironic twist. Aikman and Bond are also fascinating case studies in the strategic intersection of these two very different companies.

In acquiring James Bond, Rocky, Legally Blonde (not to mention Lord of The Rings), and exclusive rights to the NFL, Amazon is ripping plays directly from the Magic Kingdom book: amassing an IP library impervious to trends – both homegrown (LoTR) and acquired (MGM is one small part of an enormous library of content controlled by Amazon – the largest content selection of any premium streaming service) – and which appeals to the young and old ends of the audience spectrum, and everyone in between.

Conversely, Disney is building a media flywheel seemingly molded upon what team Bezos designed at Amazon. While Disney does not have an AWS generating $62 billion in revenue per year, Disney’s Parks will generate nearly as much operating income in 2022 as all of Netflix. Disney’s bundling strategy, while not backed by free home delivery, does boast deep whole-household usage. The combined audiences of ESPN+, Hulu, Hulu Live and Disney+ make Disney’s streaming as large in viewership as Netflix. Their bundle of services is priced the same or less than Netflix and has Netflix’ same low level of churn. Disney’s business global, with is 1/3 of their overall streaming audience coming from India – making them one of the only major US streamers to crack that market in a significant way. Like Amazon, Team Mickey has acquired major platforms to expand their core competencies and reach (MLBamtech, Hulu, Hotstar), has diverse revenue and audience sources (physical sales, parks, advertising, subscription), and now appears to be making their bundle of services a primary focus of their business.

The strategies shared between these two are fascinating to track. Their head-to-head match in live sports is a major driver in the entertainment ecosystem right now. Both went after Aikman. Disney won. Both are chasing the NFL Sunday Ticket, along with Apple; and both are pursuing Indian Premier League Cricket – the secret to Disney’s success in India. Both companies are also all in on the “channels business,” Amazon with Channels; Disney with Hulu Live. Amazon’s IP strategy is distinctly Disney, and Disney’s Churn lowering bundle is distinctly Amazon. Both are investing heavily in their ad business, with Amazon now leading growth in digital; and Hulu leading the ad market on CTVs, a platform on which Amazon is investing heavily.

Amazon has the fastest growing ad platform on the planet. In 2021, Amazon’s advertising platform brought in $31 billion, more than all of ViacomCBS/Paramount. First with Fire dongles and now their new Fire TVs, Amazon is the third largest aggregator of CTV streaming in the US, and a major gatekeeper/revenue sharer of all other media companies. Their Prime Membership has the benefit of the home-delivery backbone, which makes the Rundle (recurring revenue bundle) nearly churn-proof, despite a huge influx of ads on their platform. As a result, they can afford to invest heavily in the Disnification of Amazon Prime, defraying risk and accruing value across an array of businesses.

Yes, Amazon has big tech comps and Disney has OG Media comps who do numerous similar things to each. BUT… Amazon has more professionally produced and live-streamed content than any other media platform and Disney has the greatest collection of IP ever. The embedded and recurring financial loyalty both companies have with their audiences is remarkable, as is their ability to earn revenues and build audiences in moated specialty areas – parks, twitch, merch, sports.

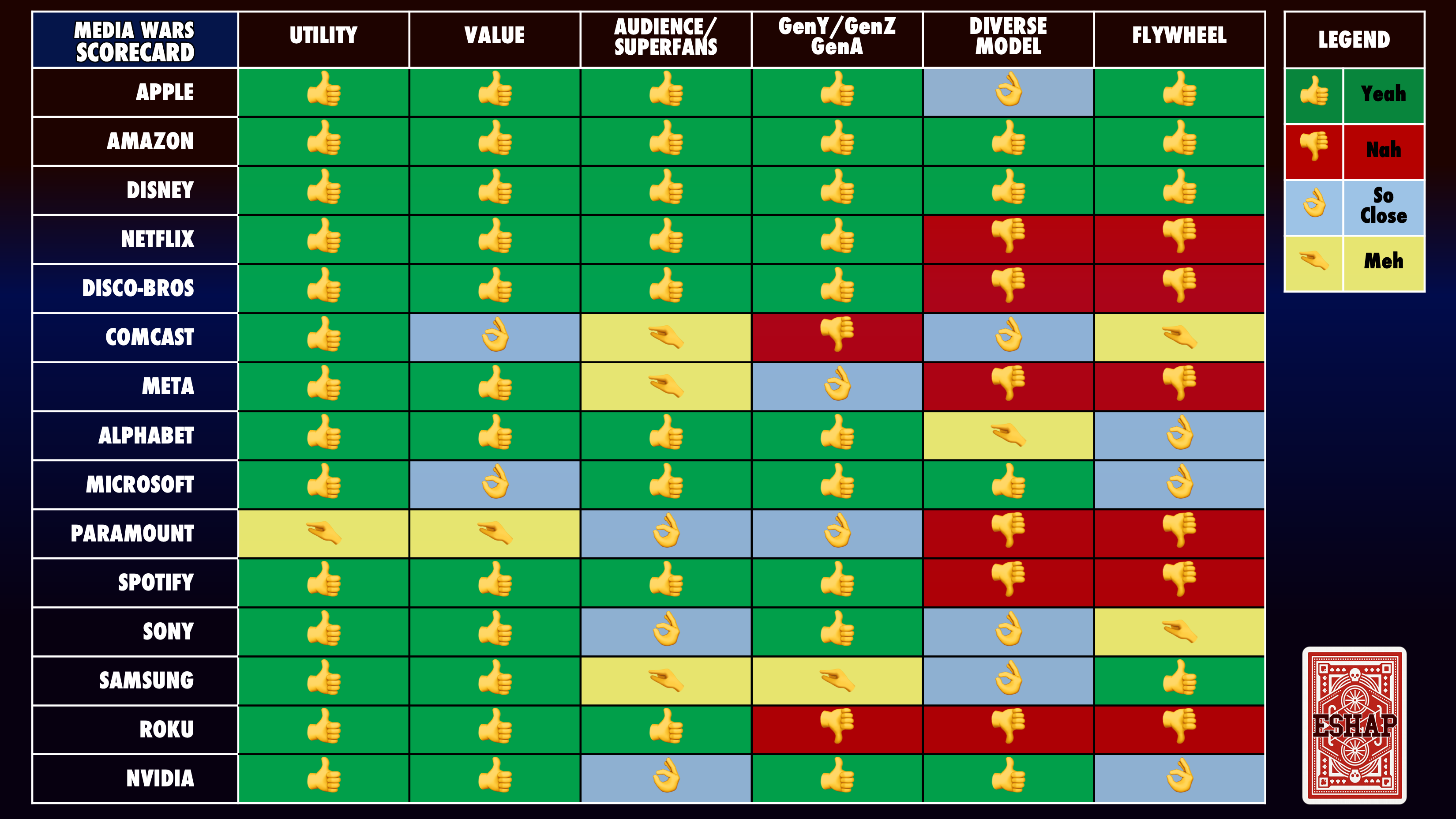

True, both are adapting a streaming TV model originally perfected by Netflix and now employed by many others. However, Disney and Amazon’s powerful and seamless mixes of subscription, bundling and advertising – combinations of single-unit sales and recurring revenue bundles – are simply not equaled by other players on the two converging ends of the modern media continuum (which is why they are the only two with 100% flying colors across my Media Wars Scorecard). The three lowest Churn services in streaming are Amazon Prime, Netflix and the Disney Bundle. They are also the three largest, in subscribers, viewership and revenues. Of those three, two make additional revenues from their viewers elsewhere on their platforms.

Amazon’s uncontested acquisition of MGM and Disney’s free agent signing of Aikman were victories for these two competitors in the #streamingwars. But as you track these two media dynasties the ways they play similarly will be as important as they ways they compete.

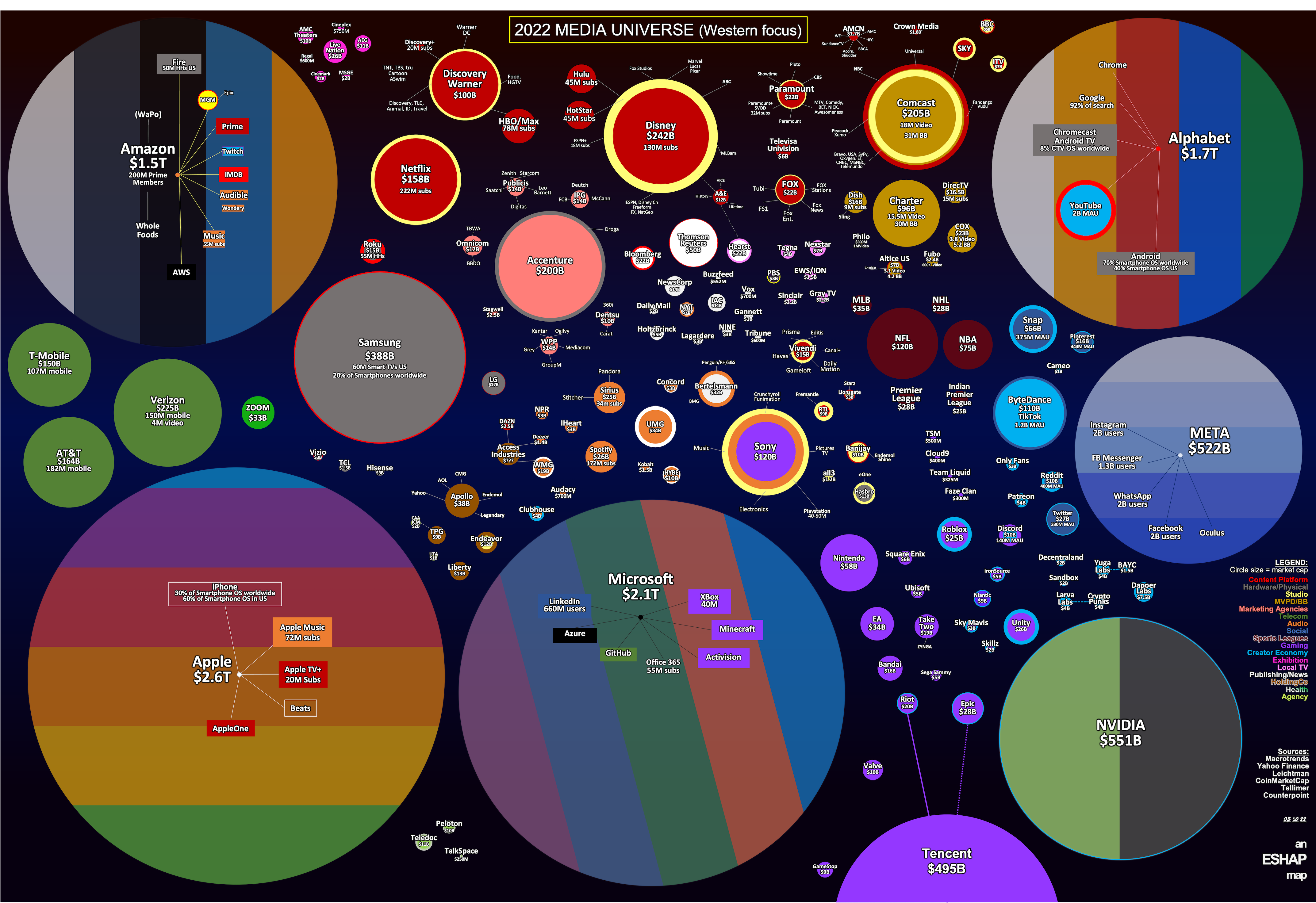

Last week at SXSW, I went through my new Media Universe Map, reshaped by the barrage of dramatic 1Q earnings and market turmoil. This Wednesday at 4p ET/1p PT, for our monthly Media WebinWar & Peace, I will dive once more into the breach for a discussion about what the wild ride of 1Q has meant for the major players, and what the now completed marriages of Amazon/MGM and Discovery/Warner will mean for those companies and their competitors.

The monthly WebinWar is for Premium Peaceniks only, and the link is below. The session at SXSW was super interactive and lively, and given the sweeping rate of change in the industry right now, Wednesday promises the same, only with less BBQ and more zoom. I hope you can join.

Enjoy the week!

ESHAP

MEDIA WEBINWAR LINK…