Grading Curve Ball

Happy Monday War & Peaceniks! School’s out and the Upfront’s over! So, it’s time to look at the state of CTV advertising, and issue grades on the this year’s class of streaming ad platforms.

Luckily last week, right in time, Antenna issued their State of Subscriptions report (card) - specifically focused on ad tiers of the major paid streamers.

While many streamers (Roku, HULU, Discovery+, Paramount+) have been in the Mad Ad Biz for years, today’s major CTV ad battles broke out last year when Netflix and Disney+ both hurriedly added ads to address massive investor fog from the streaming wars, and when the FAST craze started reaching fever pitching.

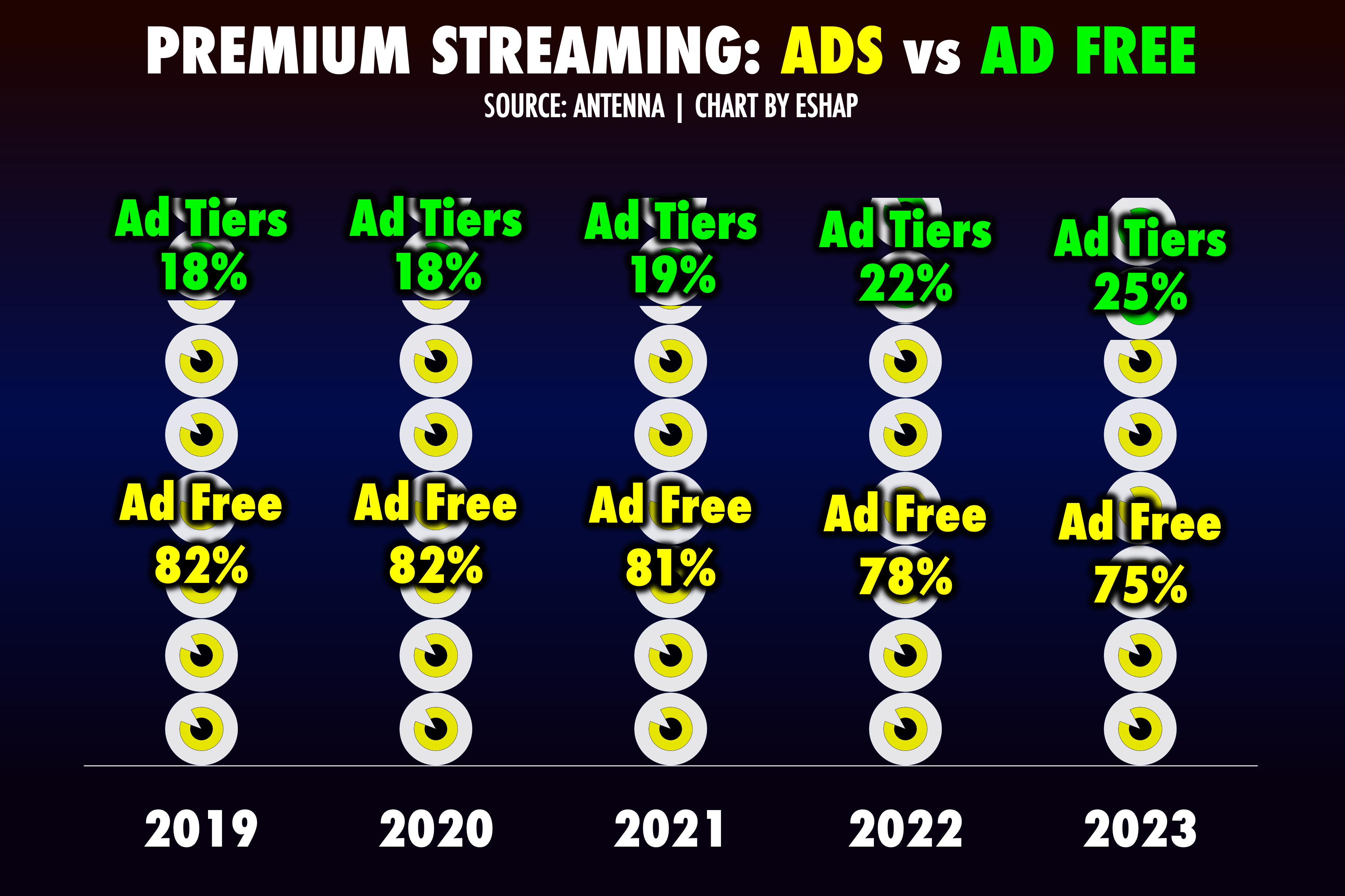

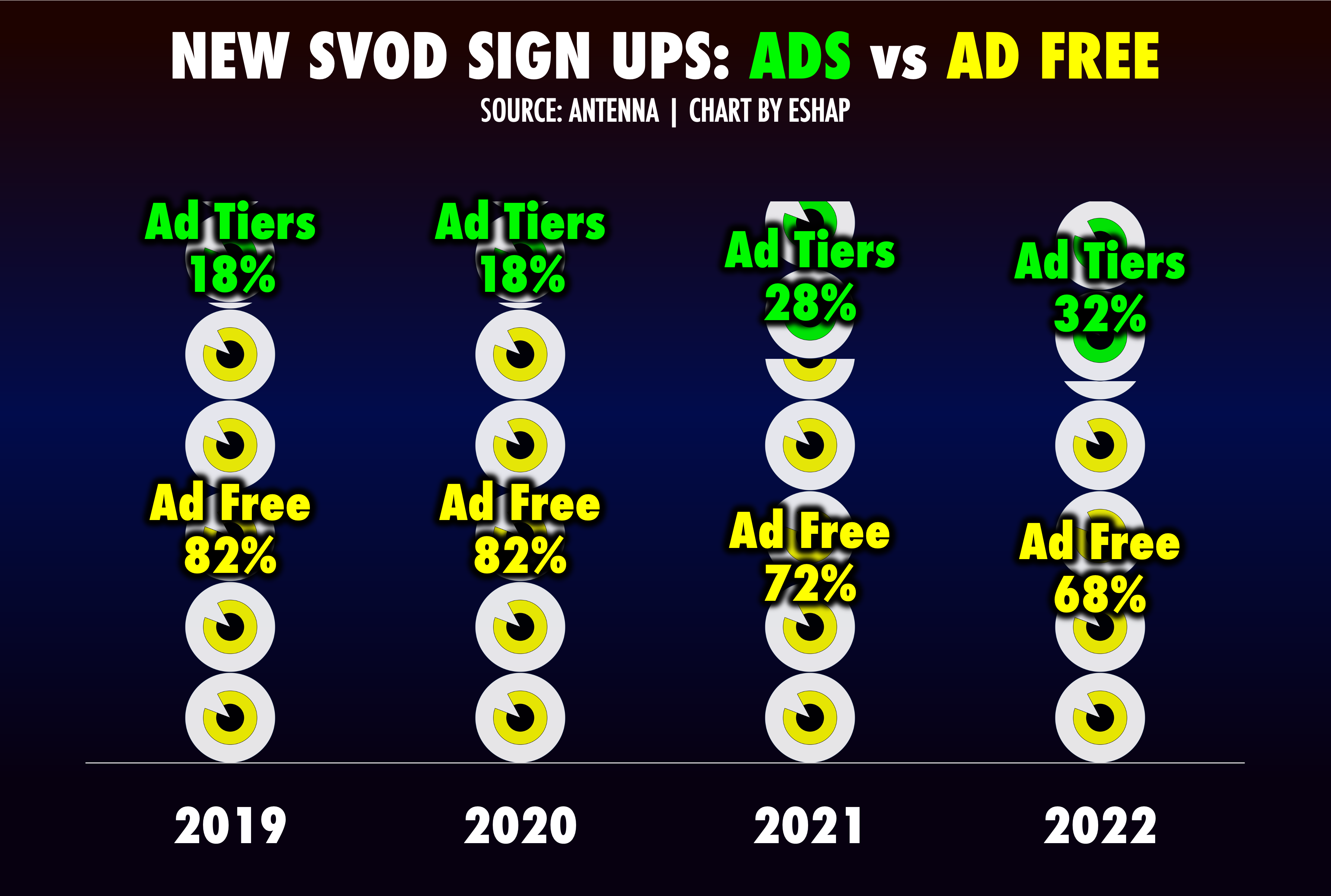

Premium streaming ad tiers are now 25% of all paid video subscriptions. More importantly, ad tier subscribers are now 1/3 of all new SVOD sign-ups.

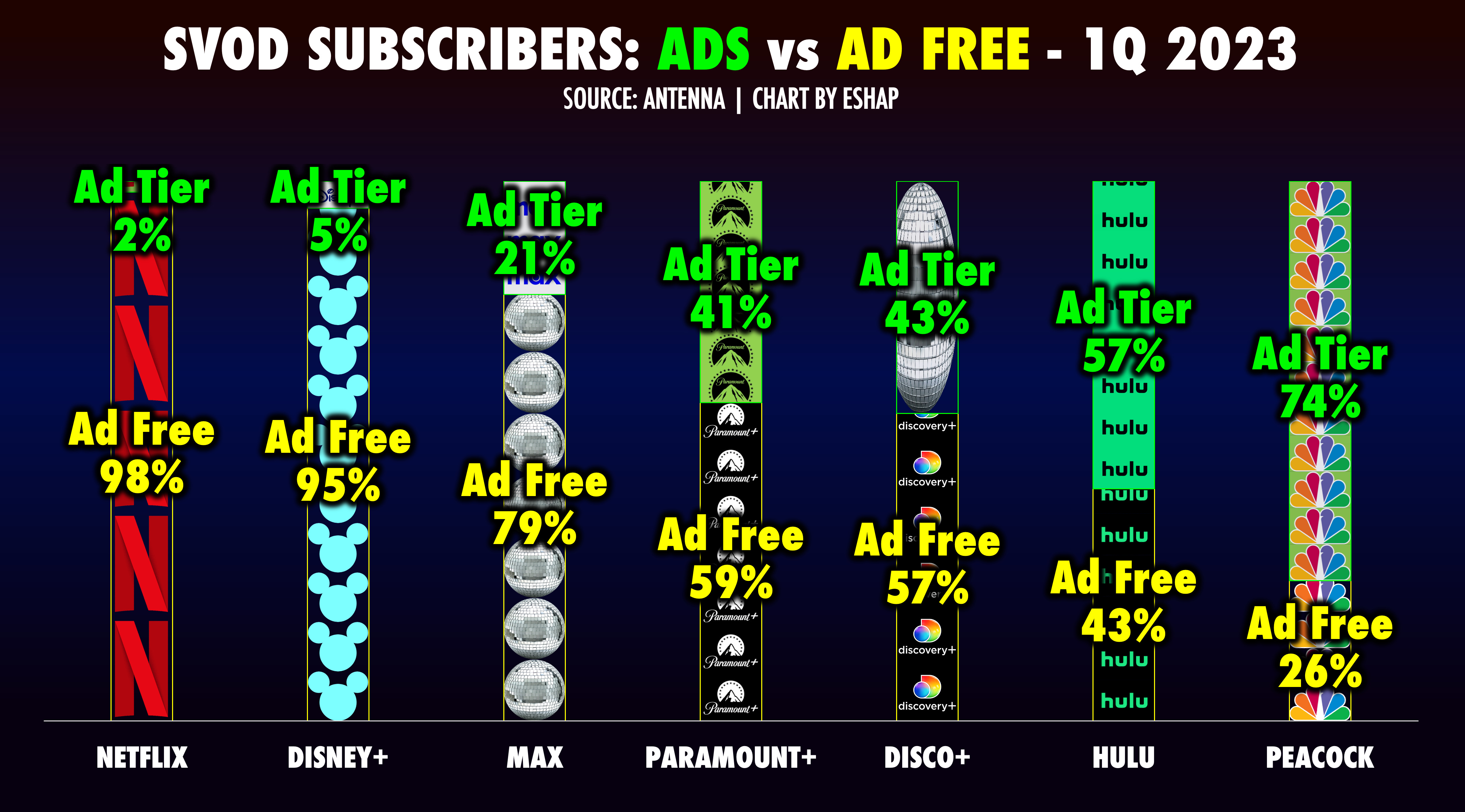

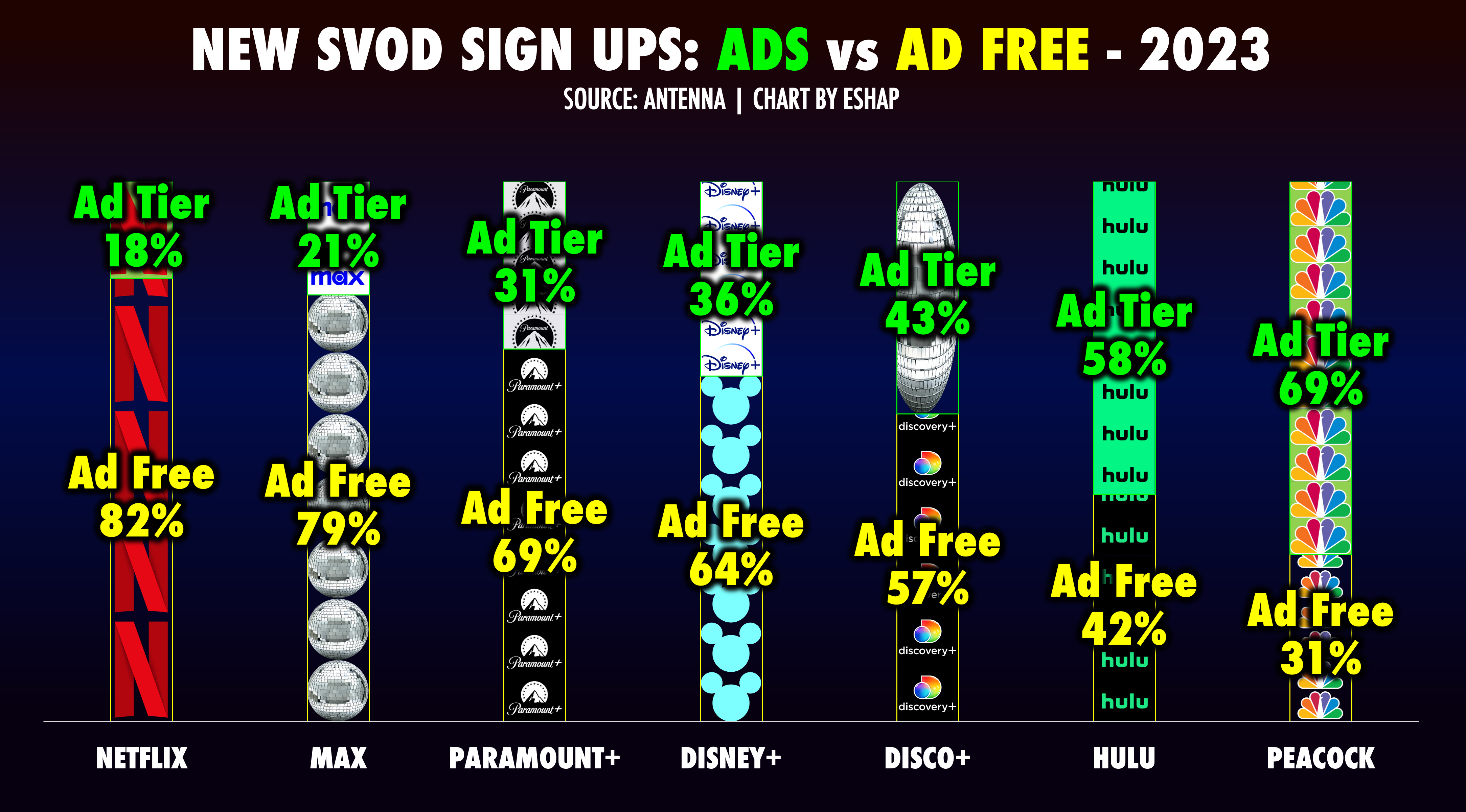

What’s also clear from Antenna’s data - based on millions of actual transactions rather than thousands of surveys - is that not all ad tiers are created equal.

Netflix and Disney hold the current lead in paid subs. But now that ARPU has overtaken scale as streaming’s key KPI, overall performance on SVOD will be judged far more moving forward on the mix of a platform’s subscriptions and revenues.

The chart above shows that some big name premium streamers still have a long way to go to reach revenue diversity, and the data below shows who’s making headway with new ad subs… and who ain’t.

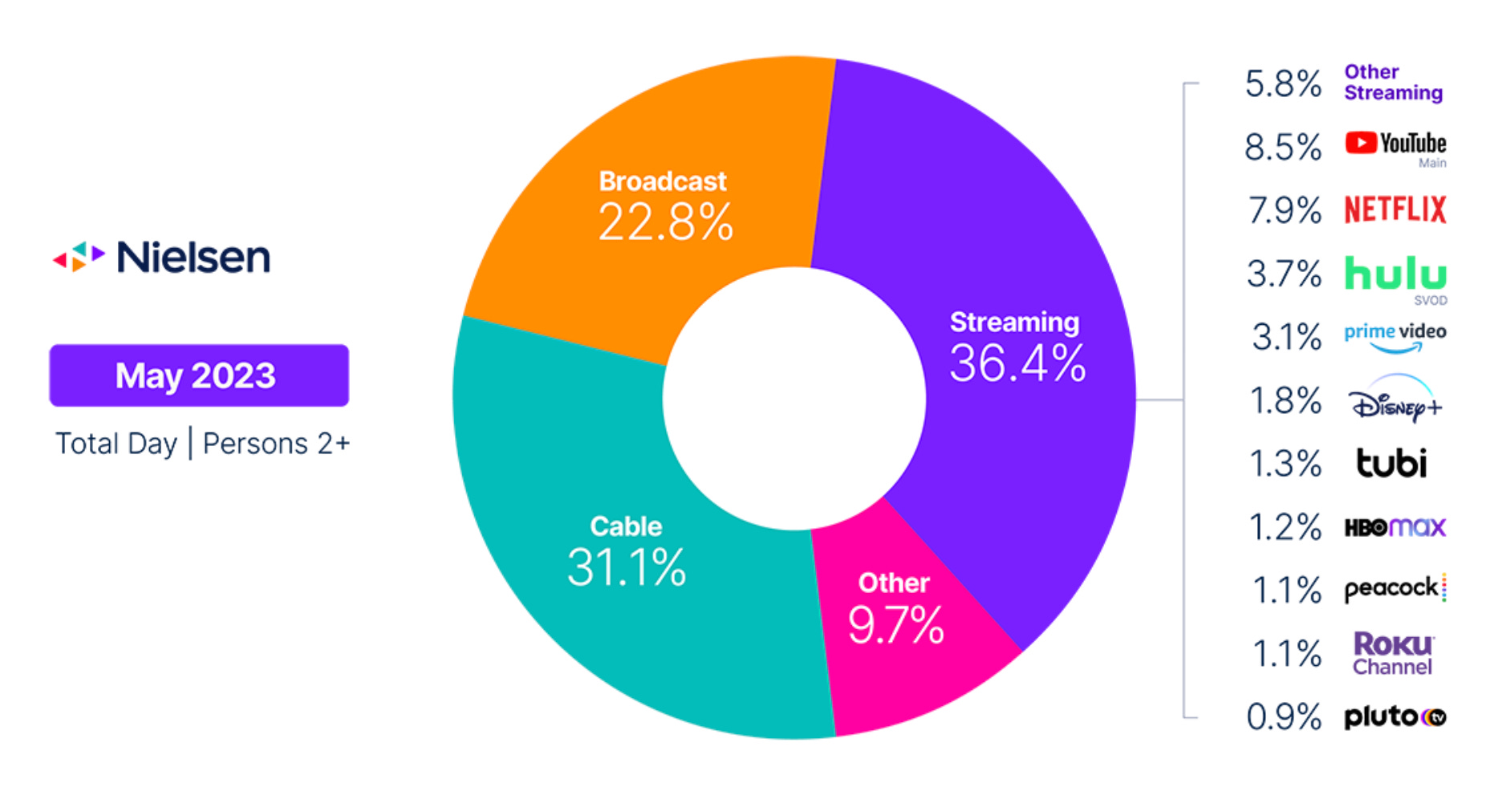

This data arrives alongside a new viewing Gauge from Nielsen, showing the FAST rise of the free streamers, with Roku Channel appearing on their measurement radar for the first time ever, with 1.1% of TV viewing.

(Before you look at their chart, please read Nielsen’s latest change of methodology, showing precisely why I take all their data with a truckload of salt.)

When you attempt to grade the various CTV ad players, as I’m about to do, it’s important to understand the entire CTV advertising ecosystem, and not just the shiny premium SVOD objects. Antenna’s data is incredibly reliable and valuable. But it does not track free services, who compete directly with SVOD ad tiers for ad dollars. With Roku, Tubi and Pluto now ensconced in Nielsen’s Top Ten streamers, the consideration set for both streaming consumers and CTV Media buyers changes bigly.

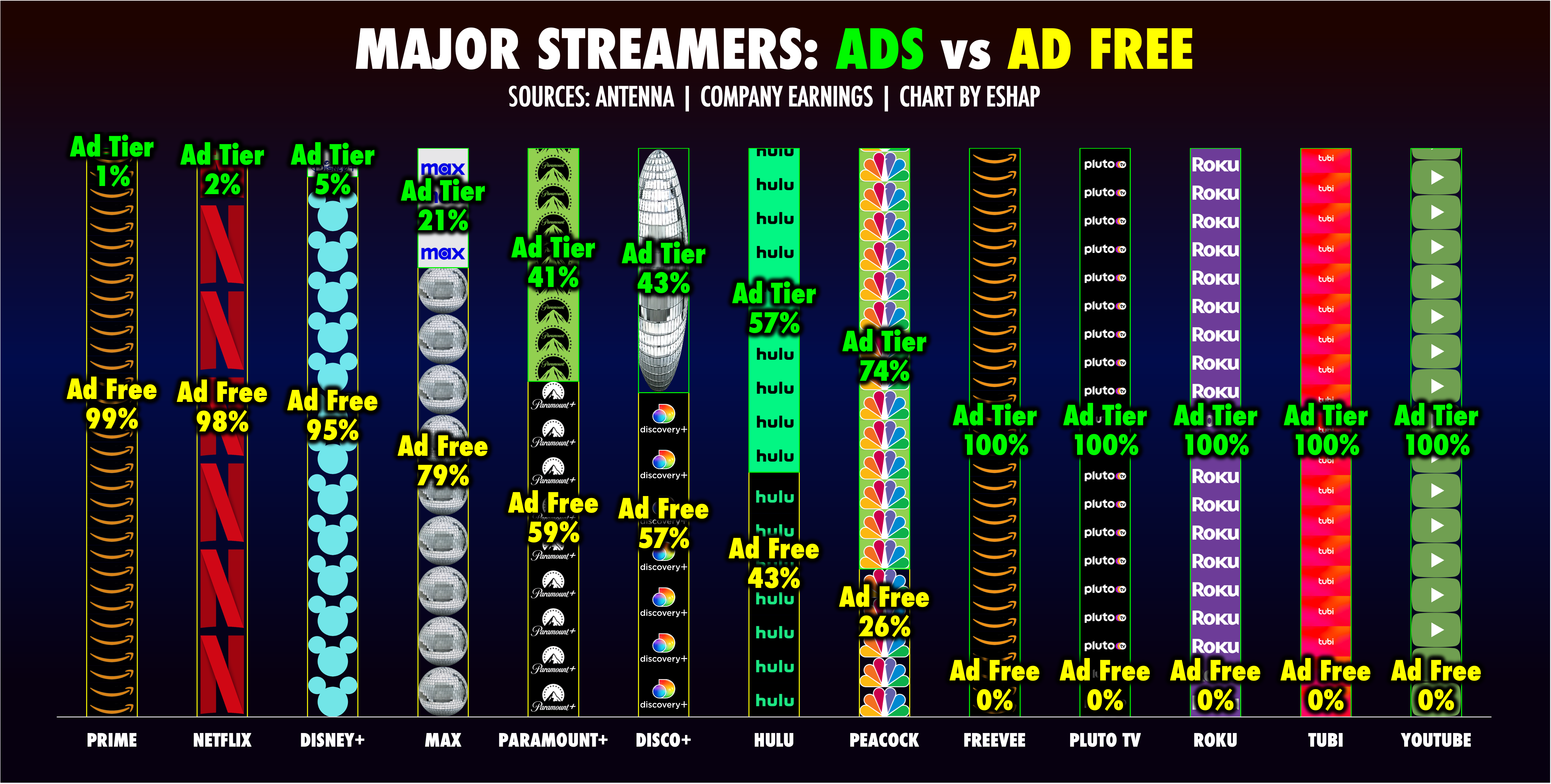

If you’re a CTV Media buyer right now, looking to place your ads, this is what you see when you window shop.

When they survey the landscape, video Media buyers must consider not just where they can buy ads, but also where their ads can be, y’know, seen.

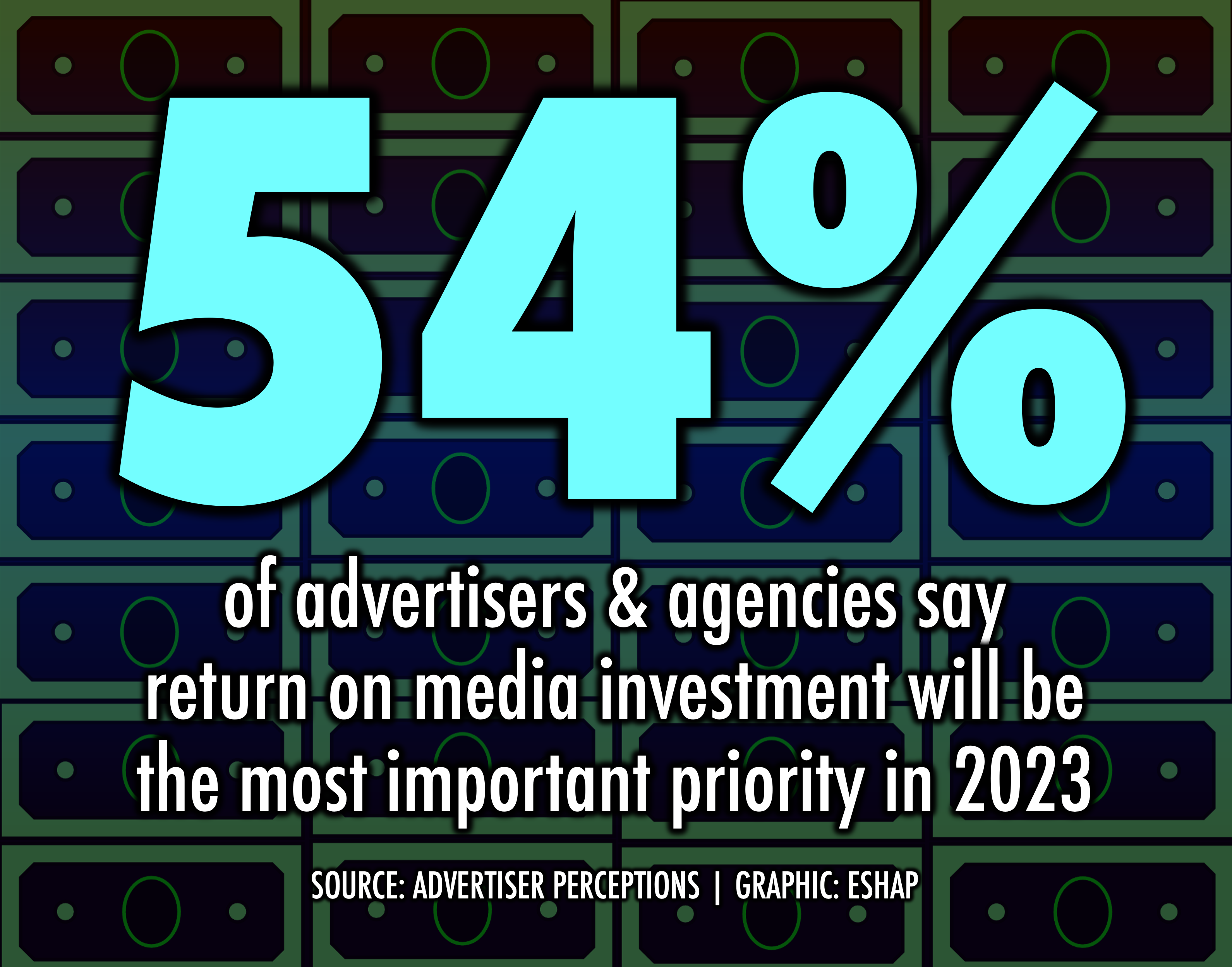

They are looking for the best economies of scale for their marketing budgets, increasingly measuring the return on their ad spend. To do that when looking at these charts, you can’t just look at individual channels, you must look at deal flow, long-term investment, and economies of scale.

Each of the platforms above are important entrants in the TV ad economy. But, in a world increasingly measured by the return on Media investments, which of the companies represented above would get the majority of your ad investment? Channels matter, but TV is a medium of scale and impact. If you were launching a movie, a truck, a new line of make-up in 2H 2023… where would you put your money, now?

That’s the approach and context I used below when assigning Media War & Peace Ad Grades (MAD Grades) to the various combatants in the CTV ad wars. Starting with Antenna’s tracking data as a benchmark, then adding context for each platform from the company who owns it, and from the marketplace itself, I attempted to handicap: Where would I spend your ad money?

You do not have to agree with any of the answers. But hopefully you’ll agree that the questions were worth asking.

Keep reading with a 7-day free trial

Subscribe to Media War & Peace to keep reading this post and get 7 days of free access to the full post archives.