CURB YOUR EXPECTATIONS

CURB YOUR EXPECTATIONS

ROKU AND ROBLOX AND TRADE DESK - OH MY!

Happy Friday War & Peaceniks! Today: Success Through Low Expectations.

The corporate bellwether of earnings season continued to ring loudly this week in the Media Universe. There was some genuine good news, even in advertising, and so much more proof that in today’s corporate hive mentality, “not as bad as you thought,” is the “pretty good” of 2023.

This is personified by Roku.

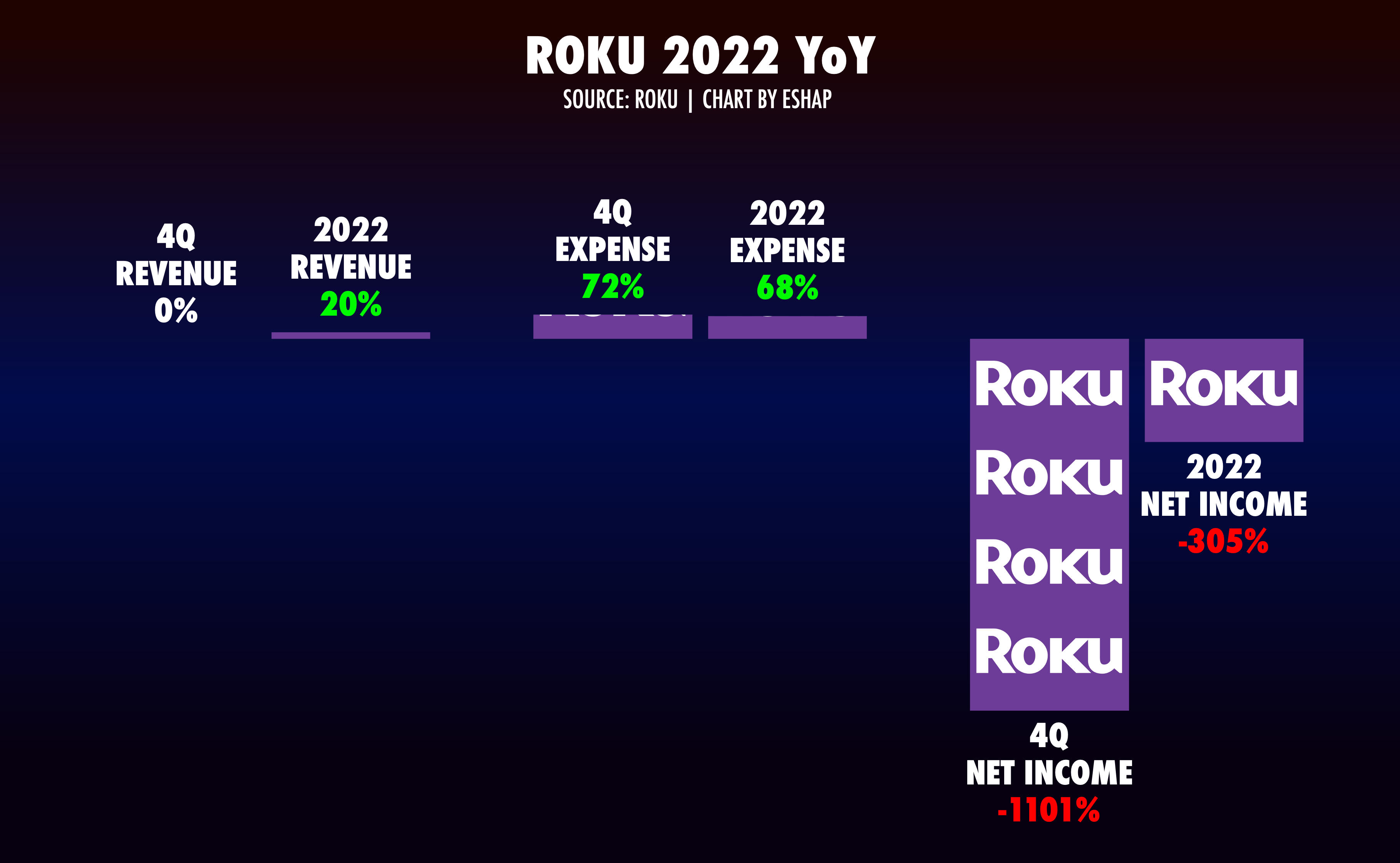

Roku announced zero percent revenue growth in 4Q with great fanfare, and was greeted with equally enthusiastic applause, and stock prices. Why? Because Roku’s numbers “beat expectations.” Their valuation is up 30% since earnings.

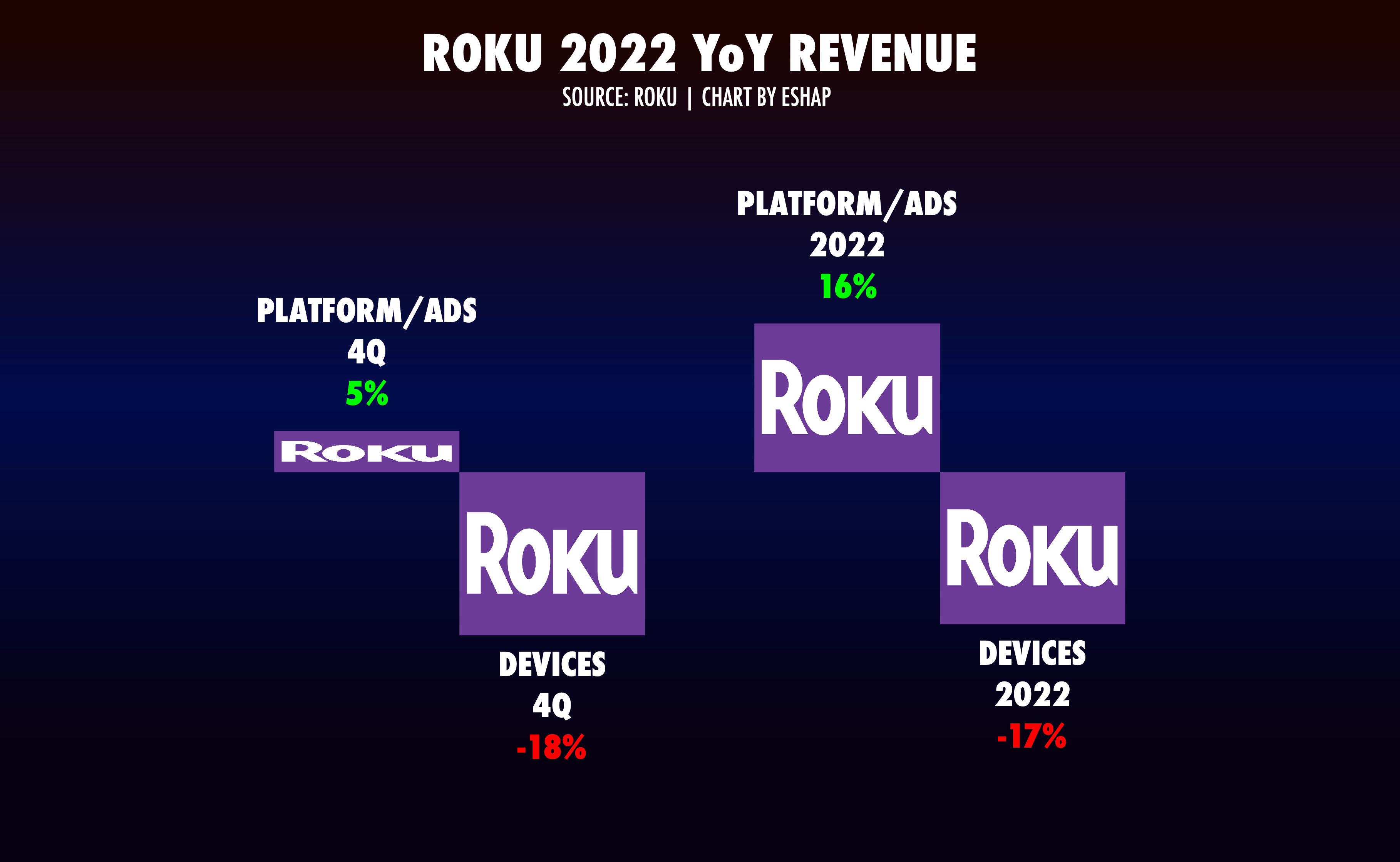

When you dig in, you see that Roku’s ad revenue actually was up 5% in 4Q, which is impressive in the middle of an ad recession. But… at what cost?

Roku’s expenses were up 72% in 4Q and 68% for the year.

Their costs actually accelerated in 4Q. This is why their net income was down 1101% in 4Q and down 305% for the year. On their earnings call, Roku’s CEO Anthony Wood told analysts "we plan to continue to improve our operating expense profile.” But he mentioned no specifics.

Let’s be clear: Roku’s revenues increased, specifically because they spent super-substantial cash on content and operations. Roku just made an expensive deal with Warner Bros Discovery for more content - unlike many of their deals which are made as revenue sharing agreements, this is license, with Roku paying Disco Bros. The current model Roku’s chasing requires more and more impressions to keep revenues growing. That growth relies on content and marketing, neither of which are going down in price anytime soon.

Roku will also launch their own line of CTVs this spring. Here’s why:

While their platform revenues - almost entirely ads - are growing, Roku’s device sales are falling faster every quarter. This is due to the migration of CTV usage from external dongles to CTVs without external devices. This is reinforced by Roku’s brag that their CTV operating system powered 38% of all CTVs sold in the US in 4Q. These CTVs are made by other companies (like TCL), who use Roku’s OS to power their platforms. So, the thinking goes, moving into the TV-making business will accelerate the growth of their 70 million account user base, and create new revenues through new device sales. But… at what cost?

CTV manufacturing is not a very profitable business. Margins on CTVs fall an average of 15% per year. And now, Roku is going into direct competition with CTV-makers who provide them with a huge part of their user base. When asked how selling a product that competes directly with their current distribution partners, Wood basically said “it’s fine.” No one on the call pressed him.

Yes, Roku “beat expectations.” Yes, their ad sales rose in a quarter where many shrank. Yes, they have a huge lead in CTV streaming in the US. BUT… their expense is exploding, and there is no clear indication that they can actually contain costs without cutting usage, and therefore revenues, to the bone. While their new CTV-making business may generate new revenues, it’s quite unclear if it can actually be, y’now, profitable. Per usual, however, after analysts heard the words “beat expectations” they asked very few hard questions, and Roku’s stock jumped up by one third.

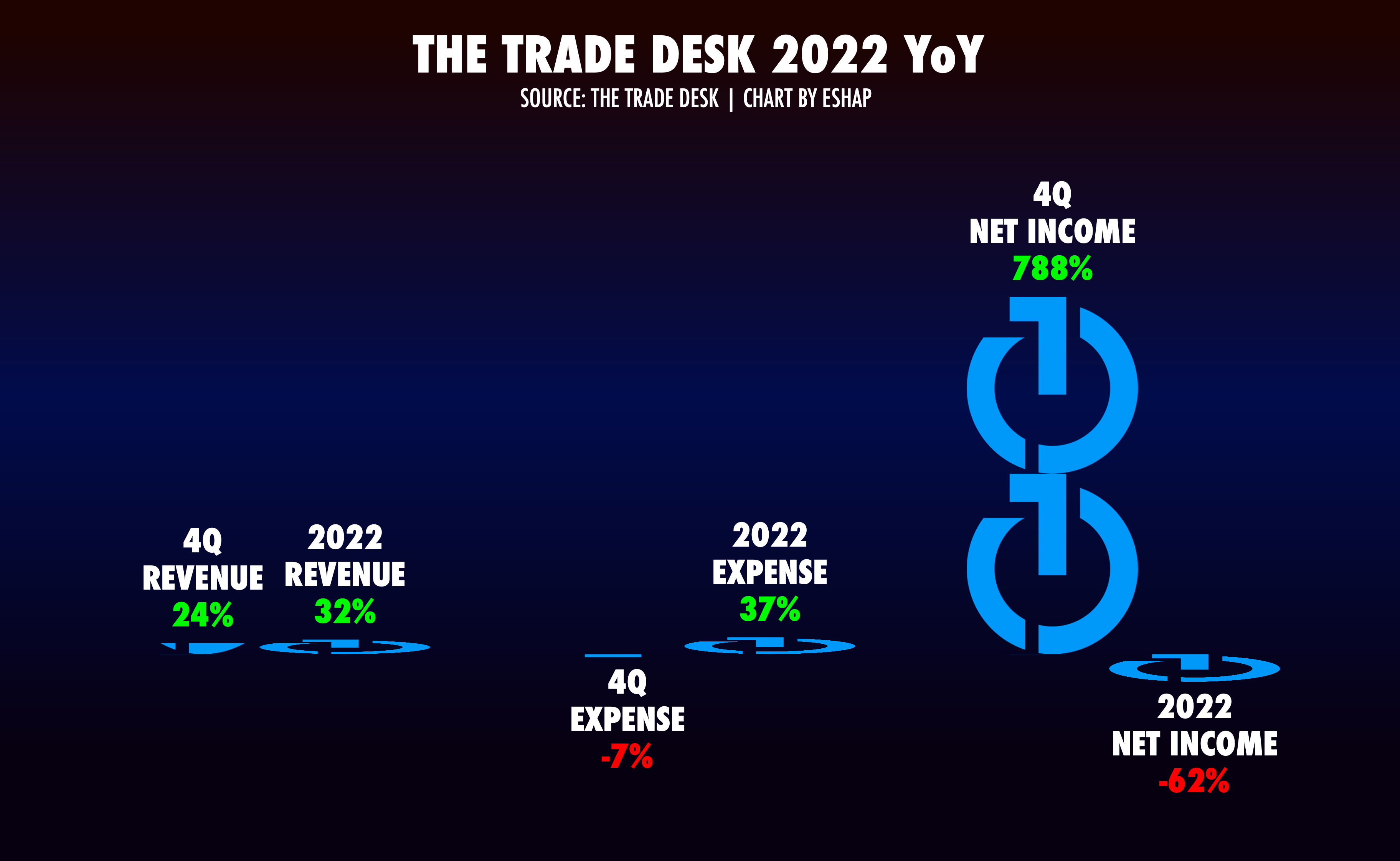

Speaking of advertising news… Let’s look at The Trade Desk.

Keep reading with a 7-day free trial

Subscribe to Media War & Peace to keep reading this post and get 7 days of free access to the full post archives.